More Good News To Fuel Equities Higher

By

Rida Morwa

By

Rida Morwa

Market Outlook: More Good News To Fuel Equities Higher

Summary

-The summer season is over. Investors and traders will be back in full force in September.

-This summer has been extremely resilient, with the markets seeing new highs almost on a weekly basis.

-Bad news was shrugged off, and investors kept buying each and every dip.

-With the new employment report being weak, the Fed is likely to remain dovish. More great news for equities!

-This great bull market is on, and it is one of the best times to be invested!

Market Outlook: More Good News To Fuel Equities Higher

We are at the end of the summer season when investors and traders get back from their vacations. Typically, market volumes are back to normal right after Labor Day.

In the meantime, this summer season was exceptional. We saw some of the lowest market volatility in my lifetime, with the markets seeing a new high almost every week. As a reminder, summer periods tend to be highly volatile due to thin trading volumes. However, the mountain of liquidity in the system has kept this bull market in full force. Even with a smaller number of players and negative news from time to time, investors keep buying each and every dip. This is the beauty of a bull market driven by excess liquidity!

Also, note that we have just entered the month of September, which tends to be one of the worst months of the year for equities. During this month, we will have a big list of economic and political issues to deal with that may increase market volatility. These issues include the "Fed Tapering", higher taxation, the infrastructure bill, and the debt ceiling.

However, the markets have shrugged off any bad news over the past 11 months, and I remain optimistic that the situation will not be any different over the next three months. We have an exceptionally strong economic backdrop fueled by low interest rates, government spending, and massive liquidity in the system. I cannot emphasize enough the impact of liquidity on all kinds of asset classes. Liquidity not only leads to increasing asset prices, such as homes, the stock markets, and bonds, but also fuels inflation. As a result, investors do not want to keep cash in their bank accounts and they keep buying assets, which further increases asset prices.

This bull market is running on very solid fundamentals and has plenty of room to run.

The Main News for the Week

The two news items that impacted the market were:

The Jobs Report, followed by the ISM PMI (Purchasing Managers Index) report. Both were released on Friday morning.

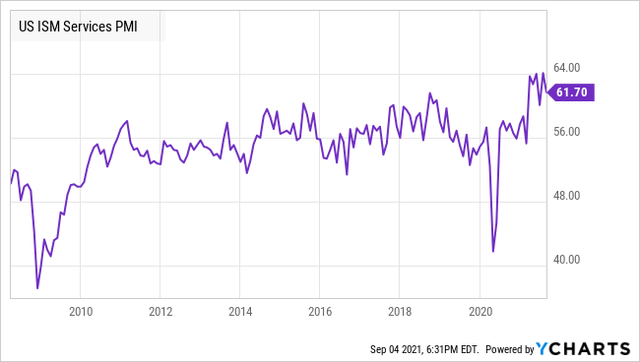

These reports had conflicting data. While the Jobs Report was a huge miss at only 235K new jobs, with consensus estimates at 733K, the ISM PMI report came in at 61.7, above the 61.5 consensus estimate. While lower than July, this is still very high.

Let us dig into these two reports to explain exactly what is happening and how the economy is shaping up.

OMG, We Lost Jobs!!!

The market started down on Friday as the disappointing Jobs Report was published before the market opened. I've seen many headlines blaming "Delta" for the poor report, and I do not believe them.

Why?

The "Jobs Report" does NOT measure how many companies are hiring; it measures how many people are hired. This crucial distinction is one that many journalists are not making. Hiring requires two things:

- An employer looking to hire and

- An employee willing to work.

Historically, during a recovery, it went without saying that workers were eager to return to work and recover from the damage the recession did to their finances. It was potential workers who were scrambling to fill a limited number of jobs. This simply is not the case this time, and multiple data points prove it.

1 - Check Out The 'Help Wanted' Signs

First, if you are not quarantining in your basement, you have likely seen signs like this one:

Open interviews every day, and this particular location was closing at 9; it was closing early because there was only one employee who showed up to work. These types of help wanted signs are becoming ubiquitous, especially in the services sector where employers are begging for employees. Many locations are adjusting hours because they don’t have enough employees to remain open.

Reading the Jobs Report on its own, one might conclude that there were massive layoffs in the food sector, as that was responsible for a decline of 42,000 jobs. The reality is, employers are hiring and are unable to find workers.

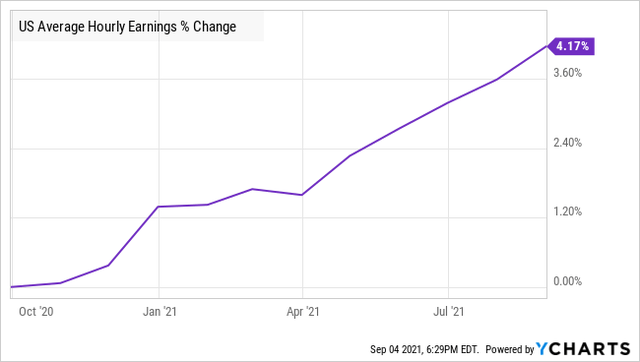

2 - Wages Are Going Up

If employers were slowing down hiring, wage growth would be slowing down. Employers offer higher wages when it is necessary to attract more workers. The Jobs Report shows that wage growth is accelerating to 0.56% in a single month. Over the past year, wages are up 4.17%, with most of that growth occurring since April.

It isn't rocket science; employers are competing to hire employees and need to offer higher wages. Not only to find new employees, but to retain existing employees. Regular readers of my Market Updates are not surprised as I have been talking about this all along. Wage growth is going to drive inflation.

And there is more to come. Walmart (WMT), PNCBank (PNC), Labcorp (LH), and Walgreens (WBA) are just a few of the publicly traded companies that have announced wide-scale wage raises that will happen this fall. These increases are not reflected in current numbers yet. As large companies raise wages, competitors will be forced to follow suit, and small companies will also have to try to compete. Wages are going up quickly, and the pace is set to accelerate.

3 - The ISM PMI Report: What Delta?

The ISM PMI (Purchasing Managers Index) is a monthly survey sent to senior executives of more than 400 companies that measures new orders, inventory levels, production, supplier deliveries, and employment. This survey is a leading indicator of economic activity.

A measurement above 50 indicates economic expansion, a measure below 50 indicates contraction.

This survey provides respondents an opportunity to make comments, and here are some of the comments from various industries:

- "Supply chain disruptions — including manufacturing-labor shortages, logistics delays and lack of material to make products — are significantly disrupting our business." [Accommodation & Food Services]

- "There is a shortage of available workers which is challenging our business operations." [Agriculture, Forestry, Fishing & Hunting]

- "Material and labor shortages continue to hinder productivity. Price increases are ever-present and repetitive. Large, multinational manufacturers have had multiple price increases in the last three months." [Construction]

You can read the rest here. There is clearly a common theme of labor shortages and minimal comment about the Delta variant.

Beyond The Headlines

It can be tempting to digest the headlines and not look at what the numbers are really telling you when reviewing economic data. Yet without context, the headline numbers can be very misleading.

The Jobs Report was a huge miss, and historically, that has been a warning sign of a recession. However, when we look at the ISM PMI report, we can see that the people in charge of running businesses identify a shortage of available workers as one of their most significant problems.

The evidence is overwhelming; the problem is not a lack of jobs but a lack of workers willing and able to work those jobs.

The Fed Is Focused On The Wrong Target

To hit your target, you have to make sure you are aiming for the right target. The Fed is not William Tell, aiming for the apple; it is Don Quixote aiming at windmills.

Last week, I highlighted Federal Reserve Chairman Jerome Powell's speech. In that speech, he emphasized that "full employment" was a condition that would have to be satisfied before tapering, a rate-hike, or other "tightening" policies would be considered.

The theory is straightforward; by keeping interest rates low, the Fed encourages/makes it easier for companies to borrow more money. By ensuring there is excess liquidity, companies can more easily expand and create more jobs. So easy monetary policy encourages more employment.

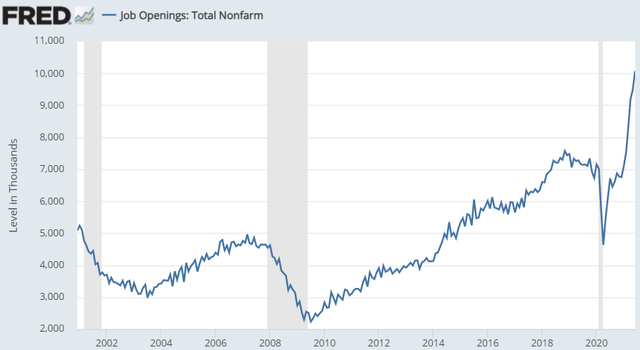

However, this theory starts with the assumption that people are unemployed because there are limited jobs. The reality? There are more job openings than ever.

Source: St. Louis Fed

The Fed has dismissed inflation as "transitory" while focusing on "full employment." The Fed can only impact the number of jobs; no Fed policy can encourage or force people to work them.

So while the Fed is tilting at the windmill of full employment, it ignores the real danger and the other half of its mandate: Inflation.

Inflation Is Here, It Will Get Worse

The Federal Reserve, the government, the news media, and the investment community are in denial. Inflation continues to have numerous tailwinds:

- Rising wages: Unlike raw material prices which will rise and fall, wages are much more "sticky." Once an employer gives a salary, it isn't easy to take it away in the future. Wages are already increasing at a swift pace, and this will continue into the fourth quarter. The weak Jobs Report is evidence that employers will be forced to raise wages even more.

- Rising rents: A lot of commercial rents have automatic increases based on CPI. We know that CPI is high, and even a stunning reversal would not be enough to keep the annual number from boosting rents for most businesses. Like wages, leasing contracts have provisions for rent to be increased; few have provisions to be lowered when CPI declines.

- A weakening dollar: The USD remained weak relative to the pre-pandemic levels and started heading back down last week. This is very bullish for commodity and energy prices. It also means that businesses will see their raw material costs remain high. The easiest way to improve the USD's strength is for the Fed to raise rates, which is unlikely to happen any time soon. The USD will remain weak well into 2022.

Source: Tradingview.com

In short, companies will see their labor expenses, rent expenses, and raw material prices rising. Ultimately, this will lead to rising prices for the consumer, which in turn will cause workers to hold out for higher wages and directly contribute to rising rents. The USD will remain weak for as long as the Fed refuses to act.

The Bubble Of Cash on the Sidelines

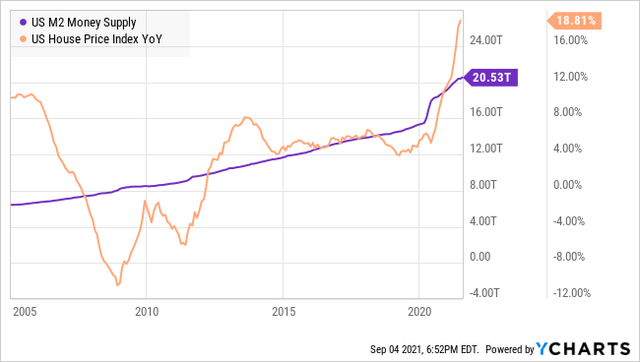

Unprecedented fiscal and monetary stimulus from the Federal Reserve has led to an exponential growth in commercial bank deposits since the beginning of the year. M2 money is the term used to measure the money supply, including cash, checking deposits, and easily convertible near money. The rise in M2 money is the most significant contributor to inflation, through changes that tend to last long.

1- Stronger Financial Health of Consumers

Government stimulus and a variety of other support measures have strengthened the financial health of most consumers. According to TransUnion’s Q2 2021 Industry Insights Report, credit card balances have decreased by 4.1% YoY. Consumers have saved more money and are paying down their credit card debt.

2- Increased Willingness to Spend

According to WalletHub research, Americans are feeling more financially secure about an automotive purchase than in 2019. Auto loan activity remains strong, with outstanding balances in Q2 growing 5.99% due to supply-and-demand issues in the automotive sector. Consumers continued to show interest in high-priced trucks and SUVs. The research also projects 87 million Americans expected to shop for a vehicle this Labor Day weekend, a figure 23% more than the number during Labor Day 2019.

We also saw higher vacation costs this summer. Vacation rentals were on average 20% higher than pre-pandemic rates - with prices at popular locations up to 50% more expensive. The absence of business travel means fewer flights in operation. This makes costs higher for those willing to travel. Similarly, rideshare companies reported that some drivers haven’t returned to work due to concerns about the Delta variant. As a result, even rideshare costs were higher for travelers.

When consumers are willing to spend more, businesses will smell the cash and not hesitate to charge higher rates. It will not be easy for this trend to subside.

3- Impact on the Investments

We keep hearing that the financial markets are overvalued across the board. When there is so much cash in everyone’s bank account, why wouldn’t they be? Since the beginning of the pandemic, CD and savings rates have been near zero. Consumers have been deploying their excess cash in the form of down payments on houses, cars, and other investments. Popular assets purchased have been soaring as a result.

- Virtual Currencies: Data from The Harris Poll shows that nearly 1 in 10 Americans used the stimulus checks to invest in cryptocurrencies, driving their prices up to record levels - Bitcoin is up 381% over the past year.

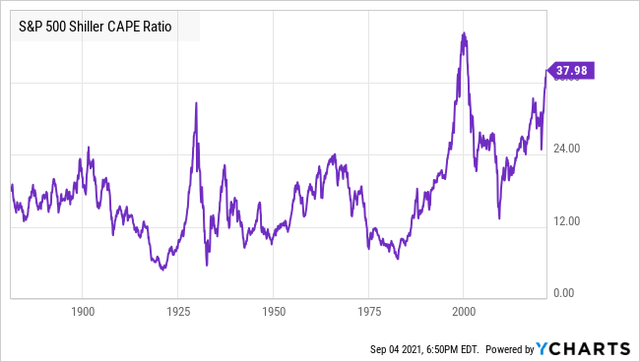

- The stock market: The Shiller PE CAPE (Cyclically Adjusted Price to Earnings Ratio) is a popular valuation measure that is calculated by dividing the S&P 500 price by the average of the earnings for the last ten years adjusted for inflation. Looking at the charts, it is clear that the stock market has also benefited from excess cash in investors’ pockets.

- Real Estate: National home prices rose almost 18% from the prior year. This level of increase is unprecedented. But unlike the GFC (global financial crisis), this time, the price rise is directly correlated with the M2 money supply in the U.S.

TransUnion’s Q2 2021 Industry Insights Report tells us that mortgage originations are on fire. We saw a 78% YoY increase in originations during Q1, indicating intense home buying activity, and the numbers stayed almost flat for Q2. These have fueled the bull market in the real-estate sector. People have more cash; mortgage rates are record-low, so everyone wants to fulfill their dream of owning a home and is willing to pay higher prices.

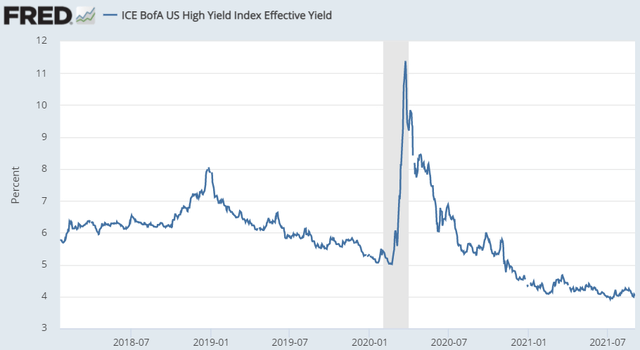

- Declining Yields: Excess cash in the system is flowing into any investment that generates yield, even if the yield is negative, considering the inflation. Look at the ICE BofA U.S. High Yield Index that is composed of sub-investment grade corporate debt (commonly referred to as "junk"). Its yield is below the inflation rate, and the consistent flow of capital into these bonds is causing the yields to drop further.

Source: StLouisFed

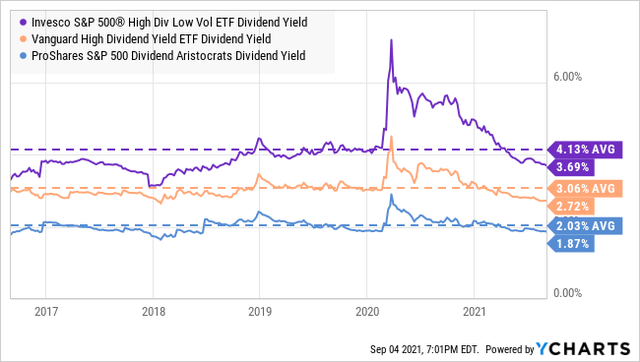

Money continues to flow into U.S. stocks and Treasuries, resulting in declining yields. Look at popular dividend ETFs like Invesco S&P 500 High Div Low Vol ETF (SPHD), Vanguard High Dividend Yield ETF (VYM), and ProShares S&P 500 Dividend Aristocrats (NOBL), to name a few. Yields are not only below the inflation rate but also below their respective 5-year average yields.

But investors continue to buy these because the inflation is so high that some yield is still better than no yield. Investors do not want their cash to sit idle in their bank accounts. Cash in the bank is trash, and most investors and retirees know this by now.

This inflation has legs. It hasn’t come up merely due to supply and demand or other transitory factors. There is a lot of cash in the system. People are willing to pay more for goods and services. As a result, merchants are ready to charge more. This shift in consumer mindset is extremely sticky in the economy and will make this inflation last much longer than the government wants you to believe.

The longer the Fed waits to act, the more extreme its actions will need to be to contain inflation.

Portfolio Positioning

The Fed will let the economy run red-hot and so will inflation. Businesses want to expand, and they have the financial means to do so. They are pushing forward with expansion even with hurdles like the labor shortage.

With that in mind, we have positioned our portfolio to "economically sensitive" stocks, and to an environment where inflation is set to remain high. We are also overweight pure "U.S. stocks" or companies that generate most of their revenues in the United States. This is because the U.S. remains the strongest economy on the globe. Never bet against America!

To check HDI's portfolio positioning click here.

The Technical Situation

The S&P 500 index broke to the upside last week, trading above the 4500 level, which is a level of resistance for the index. This is, of course, a very bullish sign. The next target for the S&P 500 index is 4600, which I expect we will reach relatively soon.

We remain in a strong uptrend line for all the major indexes, with plenty of support underneath. The first support level for the S&P 500 index is at the 4470 level which corresponds to the 50-day moving average. The second level of support is at the 4400 level which I believe would act as very solid support should we see any market turbulence. This is a market that will continue to see investors buying each and every dip with so much liquidity out there.

Note that the 2nd half of September is when most banks and financial institutions start their "window dressing" so there will be a lot of buying activity that should support equities and drive this market higher.

The Bottom Line

We remain in a powerful uptrend fueled by excess liquidity, cheap money, and strong earnings. Last week we got another confirmation that the Fed has got investors' backs and is not willing to tighten its policy any time soon, or over the next two years, which is great news for equity investors. We cannot underestimate the message that was given to us by Mr. Powell. He effectively said that the Fed will remain accommodative until the year 2023.

This week's weak jobs number is more great news for equities. This will help keep the Fed at bay because it is focused on the wrong target. No matter how much easing the Fed will do, the job market is unlikely to improve much more than this. In the meantime, the Fed will keep pumping, liquidity will remain high, driving asset prices higher. The result is that equities are the best place to be!

A dovish Fed that is ignoring inflationary pressures will keep bond and Treasury yields low, and thus make dividend stocks ever more valuable for investors seeking income. Demand for our dividend picks will continue to be high. This will result in strong capital gains in addition to our high income.

I am very excited about the prospects of our portfolio over the next 24 months, which I expect to strongly outperform! Over the next two weeks, we will have more undervalued opportunities that we will be adding to our "model portfolio" with big fat yields which will boost our overall income. Stay tuned!

===

Want to access our full report, all our top picks, and portfolio?

We invite you to take a 15-day free trial to our service. It is the #1 Service for Income Investors and Retirees. By taking the free trial, you will have access to our model portfolio targeting a +9% yield by investing in dividend stocks, bonds, and preferred stocks. Test it for yourself, I am confident that you will like it!