The Fifth Wave May Belong to the Public

By

Levi

By

Levi

A private-market thesis, a public-market handoff, and a question that may only matter in this one unique moment in time.

There is an idea I have been turning over for some time now.

It may be too esoteric to matter often. It may even be useful only for this particular moment in market history. But the shape of it has become clear enough that I think it deserves our attention.

It concerns the private companies now approaching the public markets — names like SpaceX and Anthropic — and whether their pre-IPO valuation history can be read through an Elliott Wave lens.

Let me be clear from the outset. This is not the same as counting a public stock chart.

A public chart gives us continuous price behavior. Private valuations do not. They arrive in steps — funding rounds, tender offers, secondary transactions, and negotiated marks that may or may not reflect real-time crowd behavior.

So no, I am not suggesting we treat private valuations as though they were daily price data.

But I am suggesting they may still reveal something useful: the progression of institutional conviction.

Here is the conventional observation. In many IPOs, a company comes public near the completion of a larger fifth wave of A or 1. The stock then pulls back, often sharply, as public enthusiasm exhausts itself and the structure resets. The public arrives at the top and pays for the privilege.

But what if that is not always the case?

What if, in certain rare situations, the private market builds waves ‘i’ through ‘iii’ — and the public market supplies wave ‘v’?

That is the question I cannot stop asking.

The Private Market as the Third Wave

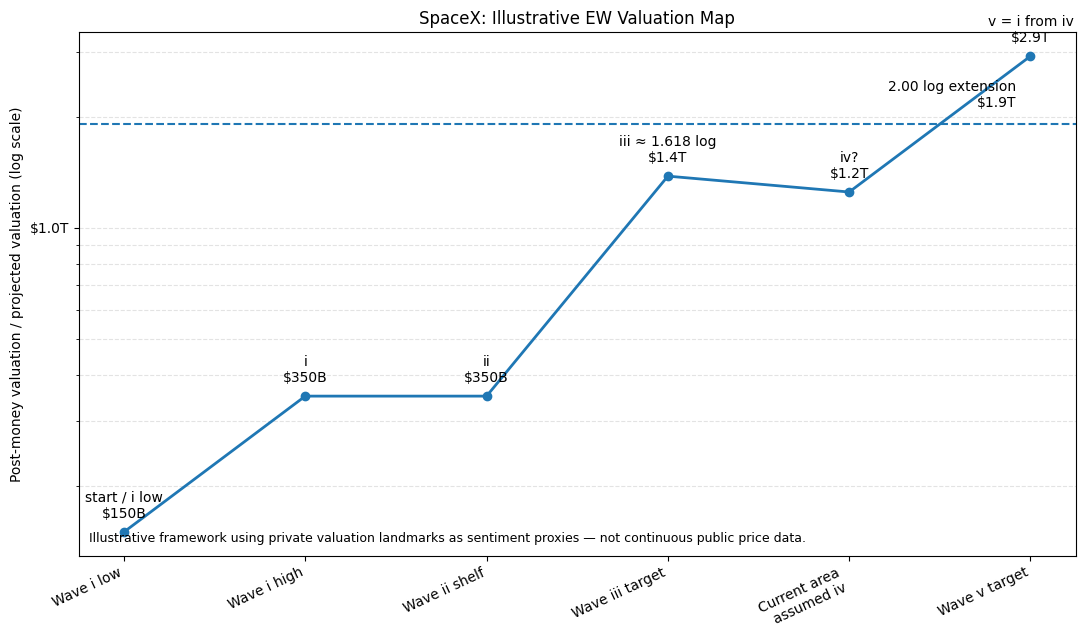

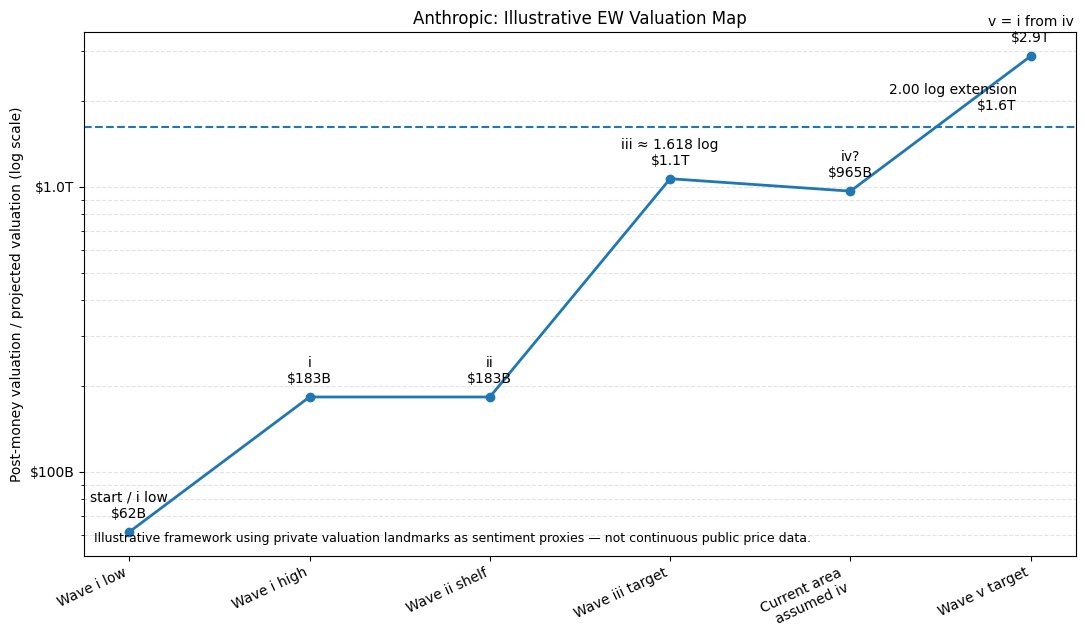

Using valuation landmarks as imperfect sentiment proxies, one can begin plotting the step-ups as a structure. Wave ‘i’ is early validation.

Wave ‘ii’ and wave ‘iv’ are not necessarily price declines, but consolidation phases — the quiet stretches between rounds, where the mark holds while the company grows into it.

Wave ‘iii’ is the major institutional repricing.

Then comes the IPO window — perhaps not the terminal top, but wave ‘iv’. The pause before the final push.

If that is correct, then the public market does not mark the end. It marks the handoff.

The private institutions build the third wave. The public supplies the fifth. And fifth waves have a very different psychology.

They are not about discovery.

They are about belief reaching the crowd — or the crowd reaching for the belief.

The Keyhole Problem

There is a complication worth confronting head-on.

The public has, in fact, already gained access to these names through vehicles like DXYZ — closed-end funds holding slices of SpaceX and, more recently, Anthropic. So the handoff has already begun, hasn’t it?

Yes and no. The public has arrived, but through a keyhole. And the behavior at that keyhole is itself a signal.

When a fund trades at a large premium to the value of what it actually holds, that premium is not rational pricing of the assets. It is sentiment leaking through a narrow opening — the public paying up for exposure it cannot otherwise get.

Think of that premium as a pressure gauge.

It does not measure the fifth wave. It measures how much demand is compressed behind the door before the door opens. A premium that runs high and stays high tells you the reservoir is full — that public appetite has not been satisfied by the imperfect wrapper, and that demand is waiting for a cleaner, more liquid instrument.

That is fuel.

When the IPO finally turns the keyhole into a door, compressed demand has somewhere to flow.

But the gauge reads both directions, and this is the part I want to be particularly forthright about. If the premium collapses before or into the IPO, it suggests the opposite — that the constrained crowd already spent its enthusiasm through the wrapper, and the listing marks exhaustion rather than ignition.

The classic pattern. The public gets unrestricted access right at the top.

So the same instrument that could confirm the thesis could also refute it. That is not a weakness. That is what makes it watchable in real time, rather than a story we tell ourselves after the fact.

I will add the necessary caveats, because the gauge is noisy. These funds carry share-issuance overhang, tiny floats, heavy short interest, and other distortions that have nothing to do with sentiment. The premium is a smudged lens, not a clean one.

But a smudged lens pointed at the right thing still beats a clear lens pointed at nothing.

The Valuation Maps

With that framework in mind, I began plotting the valuation landmarks on log scale.

Again, these are not public-market price charts. They are imperfect sentiment maps. But if the framework has any merit, the projections should not be random. We should see some form of structural coherence.

For SpaceX, using the working landmarks, the 2.00 log extension sits near $1.9 trillion, while the wave ‘v’ = wave ‘i’ projection from the assumed wave ‘iv’ area points near $2.9 trillion.

That creates a plausible interpretation in which the private market has already built much of wave ‘iii’, while a future public phase could still supply the fifth.

Not guaranteed. Not even close. But plausible enough to track.

Anthropic shows a similar rhythm.

The 2.00 log extension sits near $1.6 trillion, while the wave ‘v’ = wave ‘i’ projection from the assumed wave ‘iv’ area also points near $2.9 trillion.

I do not want to overstate the precision here. These numbers are highly sensitive to where one places the initial wave ‘i’, where one defines the wave ‘ii’ consolidation shelf, and whether the current valuation zone truly represents wave ‘iv’. In Anthropic’s case especially, the wave ‘ii’ shelf is more inferred than observed — the company has repriced almost continuously, without the clear consolidation that SpaceX printed.

But the similarity is difficult to ignore. Two very different companies. Two very different stories. Two imperfect valuation maps.

And yet both produce a potential fifth-wave zone near $2.9 trillion when the same log-scale method is applied.

That may be coincidence. Or it may be structure.

What Would Make This Useful

The thesis becomes useful only if it gives us something to watch. So what would I watch?

First, the behavior of the public wrappers. If vehicles like DXYZ continue to trade at large premiums into the IPO window, that would suggest public demand remains compressed behind the door. If those premiums collapse before the IPOs arrive, then the public may have already spent its enthusiasm through the wrapper.

Second, the IPO itself. Does the listing behave like exhaustion — a dramatic opening followed by immediate failure — or does it behave like a fourth-wave handoff, where supply is absorbed and the public market begins building a final fifth?

Third, the first meaningful post-IPO correction. That may be the tell. A controlled correction that holds key retracements would support the idea that wave ‘v’ is still ahead. A disorderly break through those levels would suggest the classic IPO exhaustion pattern is already underway.

That is where the thesis either becomes useful or dies. And that is the way it should be.

Conclusion

I am not ready to claim certainty here.

The valuation data is imperfect. The wave analogy is an adaptation rather than a textbook application. The projection math is exquisitely sensitive to where one places the launch point. And private-market marks are negotiated events, not continuous auctions.

There is also a fundamental objection worth stating plainly. These companies may list at valuations that rival public giants such as Meta or Palantir, but without the same track record of sustained earnings that helped justify those valuations.

That gap between price and profit is the bear case standing directly across from this thesis.

If the public balks at paying trillion-dollar multiples for companies still proving they can convert growth into durable cash flow, then the IPO marks exhaustion rather than handoff — and the fifth wave never materializes.

Many prior mega-listings — from Alibaba to Facebook to Arm — still allowed the public to buy in early enough to ride a meaningful portion of the advance.

SpaceX and Anthropic may be different. They may be the first examples where a larger degree third wave happened almost entirely behind the private curtain.

That is precisely what makes the question worth asking now — and precisely what could render it moot. But the idea is worth pursuing.

Because if the next wave of mega-IPOs lands retail enthusiasm on top of already massive private repricing, the final public phase may not look like a normal IPO pop.

It may look like a fifth wave. So the question is not whether SpaceX or Anthropic are “worth” these numbers in a traditional sense. That is not the exercise.

The question is whether private-market repricing has built the third wave — and whether public access may eventually supply the fifth.

That is the framework I will be tracking.

Imperfect data.

Imperfect lens.

But perhaps not an imperfect question.