Sentiment Speaks: Aren't We Here To Make Money?

All I have heard over the last year is that we are about to head into a recession – an economic construct suggesting a negative market environment. And, this has kept many quite bearish of the stock market, with most looking at the rally from 3500 to 4600SPX as the market being “wrong.” Well, I have some news for you, which was well said by the legendary Jesse Livermore:

“A prudent speculator never argues with the tape. Markets are never wrong, opinions often are.”

Yet, we have all read many analysts over the last year that were bearish for most, if not all, of the 1100-point (31%) rally. And, most of that bearishness was based upon economic theories pointing towards recession.

What caused such underperformance was that they all relied upon various economic paradigms to drive their bearish views. You see, most believe that if you understand the economics of the market, that lends itself to being able to identify financial market turning points and paths. Yet, nothing could be further from the truth.

Much of the underlying theory for economic application to the financial markets is based upon the Efficient Market Hypothesis. And, one of the cornerstones of this theory is that all investors act rationally and have the same information available to make rational decisions. In truth, I do not see the need to go beyond these factors underlying the theory for anyone with half a brain or any amount of real stock market experience to recognize how ridiculous it to be.

Honestly, are all investors making decisions based upon the exact same information? This is preposterous on its face. So, what did the economic theorists do? They modified the theory to a “weak” efficient market hypothesis in which they recognize that not all investors have the same information.

Well, to be honest, they nailed it with that name because EMH is truly weak as a market theory, at best.

But, we still are left with the claim that all investors act rationally. Another ridiculous proposition. One only has to look at a price chart to know that there is no rationality associated with the stock market movement. In fact, consider how many times you have seen the market react in the exact opposite manner (and completely irrational) relative to the logical and rational expectations maintained by the masses when news or an economic report is published. In fact, the low struck in October of 2022 was struck on such an irrational reaction, as we began this rally on a day when the CPI report came out much hotter than expected.

And, many recent market studies have outlined this anomaly through the years.

In a 1988 study conducted by Cutler, Poterba, and Summers entitled “What Moves Stock Prices,” they reviewed stock market price action after major economic or other type of news (including major political events) in order to develop a model through which one would be able to predict market moves RETROSPECTIVELY. Yes, you heard me right. They were not even at the stage yet of developing a prospective prediction model.

However, the study concluded that “[m]acroeconomic news . . . explains only about one fifth of the movements in stock market prices.” In fact, they even noted that “many of the largest market movements in recent years have occurred on days when there were no major news events.” They also concluded that “[t]here is surprisingly small effect [from] big news [of] political developments . . . and international events.” They also suggest that:

“The relatively small market responses to such news, along with evidence that large market moves often occur on days without any identifiable major news releases casts doubt on the view that stock price movements are fully explicable by news. . . “

In 2008, another study was conducted, in which they reviewed more than 90,000 news items relevant to hundreds of stocks over a two-year period. They concluded that large movements in the stocks were NOT linked to any news items:

“Most such jumps weren’t directly associated with any news at all, and most news items didn’t cause any jumps.”

Moreover, in a prior article, I have outlined that earnings are also not the primary driver of the market either:

Sentiment Speaks: How To Use Earnings To Increase Stock Market Returns

To take this one step further, many recent studies have outlined that our actions in the market are not likely driven by reason at all.

In a study performed by Dr. Joseph Ledoux, a psychologist at the Center for Neural Science at NYU, he noted that emotion and the reaction caused by such emotion occur independent and prior to, the ability of the brain to reason.

In a paper entitled “Large Financial Crashes,” published in 1997 in Physica A., a publication of the European Physical Society, the authors, within their conclusions, present a nice summation for the overall herding phenomena within financial markets:

“Stock markets are fascinating structures with analogies to what is arguably the most complex dynamical system found in natural sciences, i.e., the human mind. Instead of the usual interpretation of the Efficient Market Hypothesis in which traders extract and incorporate consciously (by their action) all information contained in market prices, we propose that the market as a whole can exhibit an “emergent” behavior not shared by any of its constituents. In other words, we have in mind the process of the emergence of intelligent behavior at a macroscopic scale that individuals at the microscopic scales have no idea of. This process has been discussed in biology for instance in the animal populations such as ant colonies or in connection with the emergence of consciousness.”

Most interestingly, other studies have shown that we do not even need information for a market to react “normally.”

In 1997, the Europhysics Letters published a study conducted by Caldarelli, Marsili and Zhang, in which subjects simulated trading currencies, however, there were no exogenous factors that were involved in potentially affecting the trading pattern. Their specific goal was to observe financial market psychology “in the absence of external factors.” One of the noted findings was that the trading behavior of the participants were “very similar to that observed in the real economy.”

When we attempt to cull all of this information into a market perspective, what we get is exactly opposite of what most believe regarding market movements. What it tells us is that exogenous information is not likely having the effect upon the market that many believe (as one study showed us it was not even needed), as the market is more likely driven by biologically driven emotion directed by herding rather than by rationality.

Yet, despite the empirical evidence to the contrary, much of what we read about in the market stems from a “rationality” theory, as driven by information, weakly or otherwise.

In fact, I just read an article that claimed that higher rates and the US Dollar caused the recent decline in the stock market. While it’s a nice story and likely to be believed by the masses, unfortunately the storyteller was not burdened by the actual facts or empirical evidence. You see, interest rates were almost at the exact same level in October 2022 when we were hitting the 3500 lows as they were at the end of July when we were hitting the 4600 highs. As far as the dollar, well, one simply has to look at a long-term chart of the dollar to know that it has been in a long-term uptrend alongside the stock market since 2011.

What I also find so interesting is that authors readily explain why they believe a market moved in a certain direction after the move occurred. Oftentimes, they use some of the same “logic” as I just noted in the paragraph above. Yet, why are they never able to tell you it will happen before it does? The simple reason is because they are only rationalizing a move after the fact, but do not have the real tools to see it with foresight.

During recent times, more and more people have begun to move away from this traditional perspective of market theory. And, rightfully so. In fact, Benoit Mandelbrot (another of the progenitors of EMH) outright stated that one cannot reasonably apply an economic model to the financial markets:

“From the availability of the multifractal alternative, it follows that, today, economics and finance must be sharply distinguished . . .”

And, if you are still unconvinced, in January of 2010, Eugene Fama, the father of the Efficient Market Hypothesis, told the New Yorker:

“I’d love to know more about what causes business cycles. I used to do macro-economics, but I gave up long ago. Economics is not very good at explaining swings in economic activity. We don’t know what causes recessions. We’ve never known.”

Yes, my friends, feel free to read that again. The father of EMH came out and told us that it does not work, and he gave it up long ago.

Yet, the Efficient Market Hypothesis is not only still taught in colleges today as the underlying theory for markets, but most of the market analysis you read stems from this perspective. And, when economists are presented with the question of empirical failure, the common answer given by honest economists is that they simply have nothing better.

As the January 6, 2011 issue of Oxford Analytica explained:

“Paradigm shift? It is premature to conclude that there is some fundamental change in economic thinking at work. Paradigms are not discarded unless there is another paradigm to replace them. . . Although the crisis has exposed serious weaknesses in the neoclassical synthesis, no alternative paradigm is likely to eclipse it in the short term. Moreover, there are strong intellectual and social pressures at work to hold the paradigm in place.”

What other “science” continues along a path that is recognized by most as inadequate? To date, we still debate the cause of the Great Depression, the October 1987 market crash, the Asian financial crisis, the 2010 Flash Crash, and many other “anomalies” in the market. I fact, in 1997, a Nobel-prize-winning economist noted that “[t]he truth is that nobody really imagined that something like the Asian financial crisis was possible, and even after the fact there is no consensus about why and how it happened.”

As Mr. Prechtor appropriately noted in The Socionomic Theory of Finance:

“Can you imagine physicists endlessly debating the cause of avalanches? . . . Economists are mystified over the causes of market declines and economic contractions because they are using a mechanical model in the realm of finance where it doesn’t apply.”

Recently, we experienced the exact opposite, wherein the market rally from 3500 to 4600 mystified those using the same mechanical economic models.

While I am only touching upon one aspect of the economic theory underlying most market analysis, I think I have made my point. In fact, I could probably write another 20-30 pages taking apart many other aspects of this “theory,” but I do not think that to be necessary for our purposes here.

If you are interested in a much deeper study of this perspective, I strongly encourage you to read The Socionomic Theory of Finance (from which much of the research cited herein has been compiled), which is a groundbreaking volume in its depth and breadth of analysis of the current paradigm, as well as its focus upon a proposed new paradigm.

So, if our goal is to make money in the market, should we be relying upon economic paradigms to guide us? Should you be relying on any analysis which presents economics as the basis for a prognostication?

What I personally find quite amusing is that many of those who rely upon economic paradigms for their market perspective view my work as nothing more than “magic” or “voodoo.” I always find it amazing that, despite them being wrong so often, they still have the audacity to negatively opine about a market analysis methodology they admittedly do not understand. Moreover, one would assume that the old adage “pain instructs” would be applicable to adjust their perspective. Apparently not.

As Albert Einstein once noted:

“Few people are capable of expressing with equanimity opinions which differ from the prejudices of their social environment. Most people are incapable of forming such opinions."

Or, we can look to the famous words of Lord Francis Bacon:

“The human understanding when it has once adopted an opinion (either being the received opinion or as being agreeable to itself) draws all things else to support and agree with it.”

I think Daniel Kahneman may have said it best when he noted that we have a puzzling limitation within our minds: “our excessive confidence in what we believe we know, and our apparent inability to acknowledge the full extent of our ignorance and uncertainty of the world we live in. We are prone to overestimate how much we understand about the world . . overconfidence is fed by the illusory certainty of hindsight.”

Well, ask those that have come to learn what we do so differently than the masses, the curtain is pulled back, and the wizard’s truth is revealed as not having any “magic” or “voodoo” at all:

“For too many years I thought EWT was voodoo…. Not anymore . . . I know I fought this.. but damn it works . . . My accounts are killing it.. returns I did not think possible.”

As far as my current market views, well, as I explained in my article last week:

“I believe we are approaching a near-term bottom, which will then set up a rally over the coming weeks or months. I am not sure exactly how long the rally will take, but I am targeting the 4350-4475SPX region as of right now.”

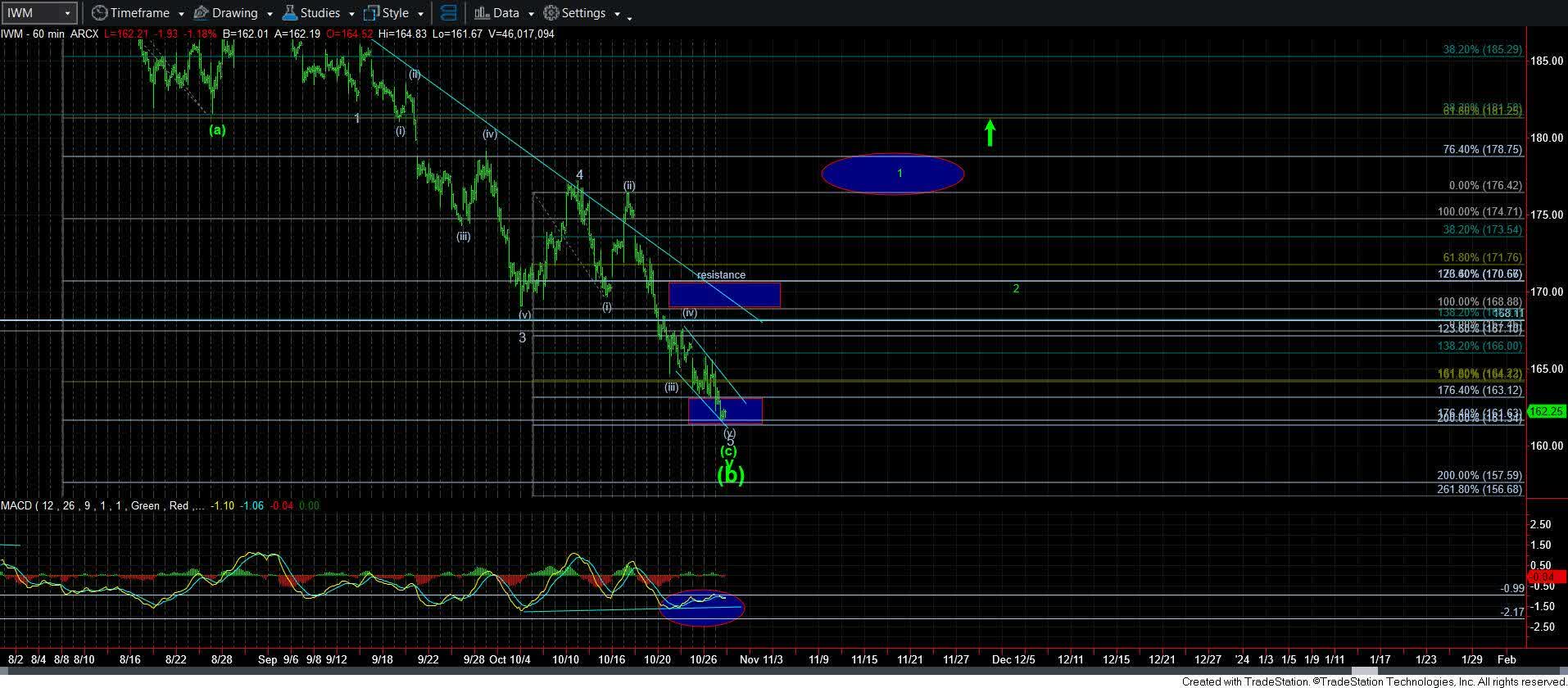

In fact, this was my chart for the IWM at the end of the prior week. And, as you can see, we have now just about reached my initial target in that as well.

Elliottwavetrader.net

Now, in truth, I did not expect that we would get to my target within a week. But, oftentimes, when the market gets extremely oversold, we do see the resulting initial move off the lows form a parabolic-type of rally. This is what we experienced over the past week.

So, does that mean we are preparing for a market crash? The answer is not yet. You see, many have not gone beyond the title of my last article, and have misinterpreted it to believe that we are certainly going to crash and that I have gone bearish. If you read the article carefully, you would know that I said that the environment is now ripe for a market crash set up to develop. This is no different than when we say that the weather conditions are such that a tornado can develop. Does that mean it will develop?

I think the next 2-3 weeks will likely tell us if the market is going to set up a crash, or if we are going to still rally to the 4800SPX region before that major bear market I expect in the coming years takes hold. So, I am going to reserve judgement until I see how the market takes shape over the coming week. But, I will say that should I see a 5-wave decline begin at any point in time from now, then I will likely be preparing for a potential market crash. Until such time, I am giving the market the opportunity to provide me the set up for another major rally phase into 2024.