Amazon’s Rally May Be Farther Along Than It Looks

By

Levi

By

Levi

Amazon is not limping into this discussion.

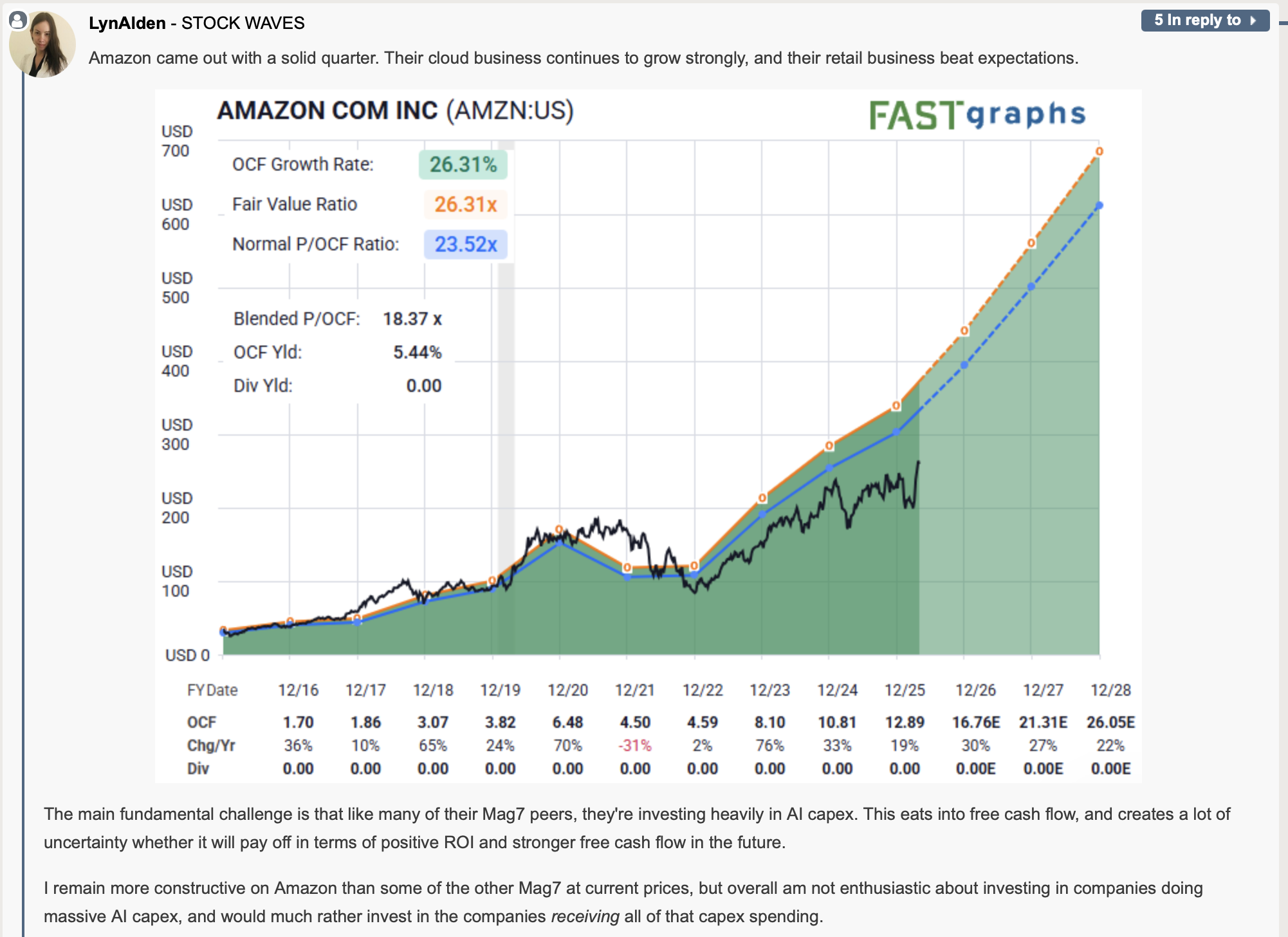

The company recently delivered a solid quarter. Cloud continues to grow. Retail beat expectations. The operating picture is not one of deterioration or distress. If anything, among the Mag 7 names, Amazon still carries one of the more constructive business profiles.

But stocks do not always wait for the business story to weaken before the chart begins to change character.

Sometimes the business looks strong while the stock’s advance is already maturing. That is where this setup becomes interesting.

Lyn Alden recently framed the fundamental picture in straightforward terms:

“Amazon came out with a solid quarter. Their cloud business continues to grow strongly, and their retail business beat expectations.”

That is the favorable side of the ledger.

The company still has multiple engines. AWS remains a major profit driver. Retail has regained operating credibility after years of margin pressure. Advertising continues to provide an additional high-margin layer. Amazon is not a one-product story, especially when investors compare it against other mega-cap technology names.

But Lyn also highlighted the central challenge:

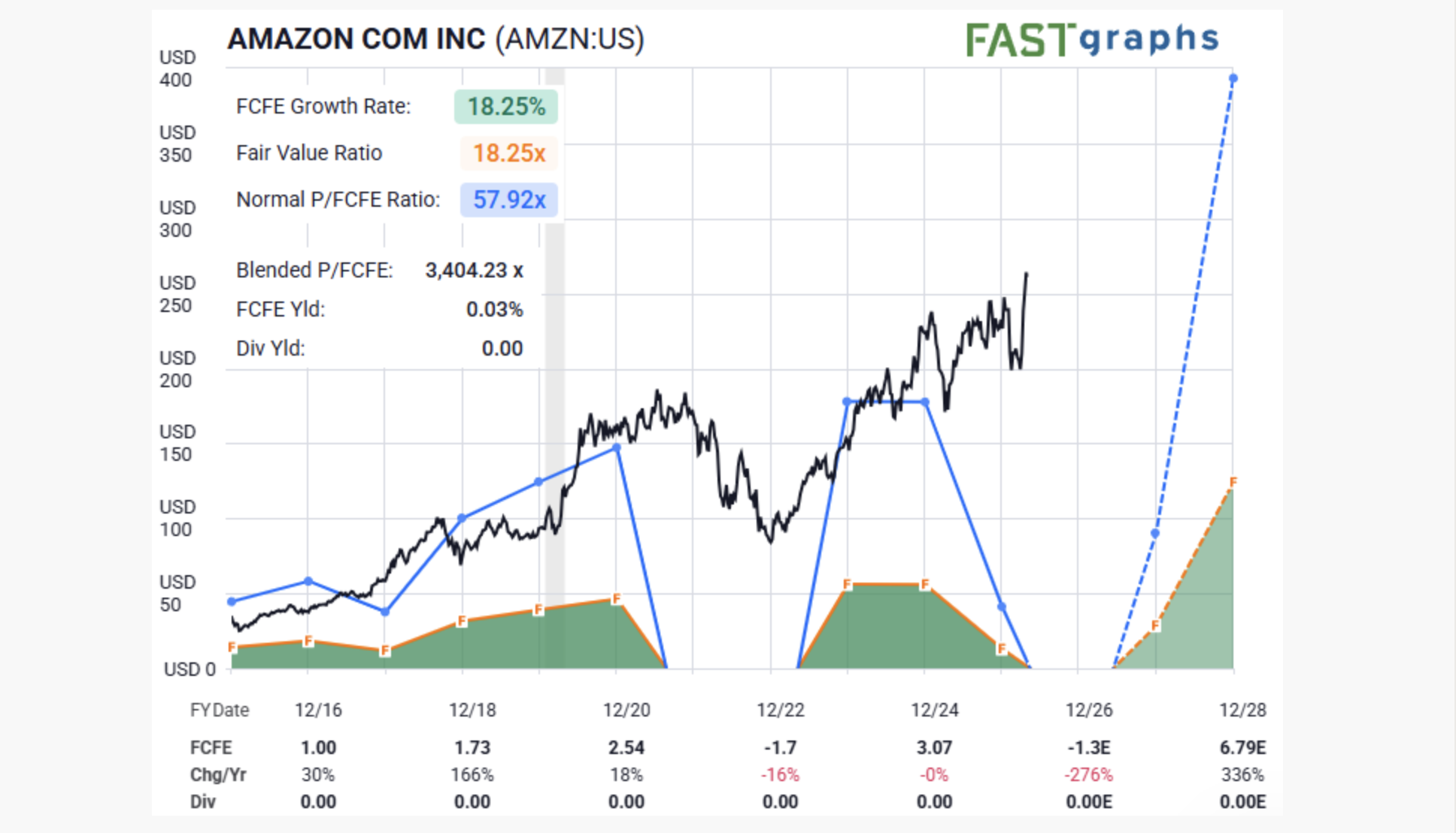

“The main fundamental challenge is that like many of their Mag7 peers, they’re investing heavily in AI capex. This eats into free cash flow, and creates a lot of uncertainty whether it will pay off in terms of positive ROI and stronger free cash flow in the future.”

That is the tension.

Amazon is still executing, but it is also spending heavily into the AI buildout. The market may ultimately reward that spending if it produces durable future cash flow. Or it may decide the bill is arriving before the payoff is visible enough.

Lyn’s conclusion is measured:

“I remain more constructive on Amazon than some of the other Mag7 at current prices, but overall am not enthusiastic about investing in companies doing massive AI capex, and would much rather invest in the companies receiving all of that capex spending.”

That is a fair fundamental frame. Not bearish. Not euphoric. Constructive, but cautious.

And that brings us to the chart.

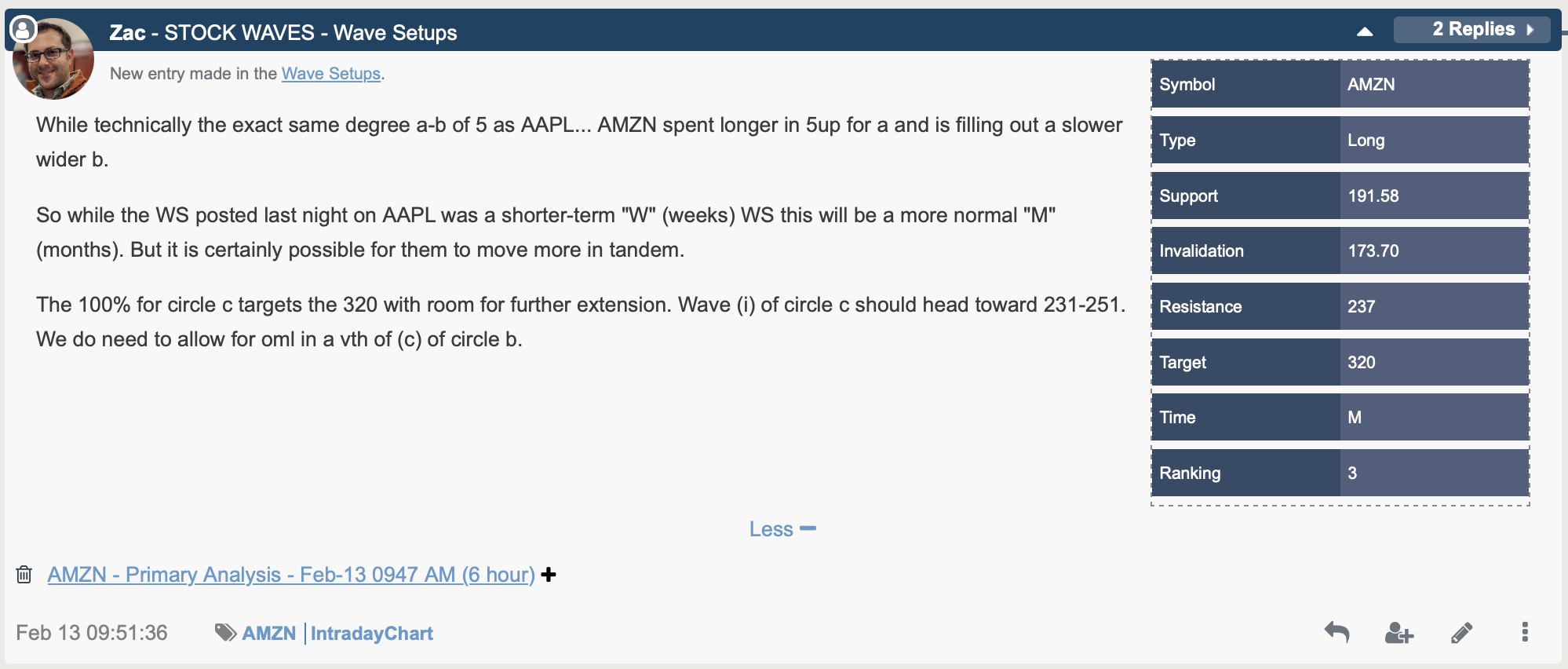

Zac’s original February wave setup on Amazon has worked very well so far. The stock was identified as a long setup, with support near 191.58, invalidation near 173.70, resistance near 237, and a larger target around 320.

Since then, price has done what strong structures are supposed to do. It moved.

The rally has not been shy. It has not offered much in the way of comfortable pullbacks. It has simply pressed forward, and that kind of behavior can feel validating for anyone already positioned.

But this is where we need to slow down for a moment.

Where Are We in the Structure?

A rally that refuses to pull back can be bullish. It can also be a clue that price is farther along in the larger structure than originally assumed.

Those are not the same thing.

Elliott Wave analysis forces us to ask a different question. Not merely: “Is the stock strong?” But: “Where are we in the bigger context?”

Because if Amazon is already advancing through the later stages of circle ‘c’, then the next major upside region is no longer just a target. It becomes a potential completion zone.

That is why the 293–320 region now deserves close attention.

The 100% extension for circle c points toward the 320 area, with room for further extension if momentum persists. Before that, price may still need to work through intermediate resistance and smaller-degree subdivisions.

So, yes, the chart can still support higher prices. But the message is more nuanced than simple upside. Amazon may not be early in the move anymore.

That is the point.

If the stock reaches the 293–320 zone in the current structure, it could mark something more meaningful than another stop on the way higher. It could represent an important high — perhaps one that leads to a multi-month, or even multi-year, corrective phase once the advance completes.

Large corrections can begin while companies still look fundamentally healthy. In fact, they often do. The headlines do not need to turn negative first. Earnings do not need to collapse. Analysts do not need to downgrade in unison.

Price can finish a structure while the story still feels comfortable. That is often how important highs form.

Amazon’s case is especially interesting because the fundamental and structural pictures are not in conflict. They are both saying something similar, just in different languages.

The business is strong, but the AI capex cycle introduces uncertainty. The stock is strong, but the advance may be maturing. Both can be true at the same time.

For investors, the practical takeaway is not to suddenly turn bearish on Amazon. The company remains one of the highest-quality businesses in the market, and the current structure can still carry higher.

The better takeaway is to recognize where risk may begin to change shape.

Below the surface of a strong rally, the stock may be approaching a zone where upside reward becomes less clean and the next corrective phase begins to matter more.

That is not a reason to panic. It is a reason to pay attention.

If Amazon continues higher into the 293–320 region, we would not treat that simply as proof that the bullish story has become stronger. We would treat it as a region where the structure may be nearing completion.

Strong company. Strong rally. Maturing structure. That is the combination.

And if price reaches the upper target zone, the most important question may no longer be how high Amazon can go.

It may be how much of the advance was already spent getting there.