Yield Curve Inversions Deepen

As the inflation cycle downturn and the growth rate cycle downturn persist, with the Fed seemingly unwilling to guide towards a more aggressive rate-cutting path, yield curve inversions have intensified.

The spread between the 10-year and 2-year Treasury rate has fallen to -5bps, the deepest inversion of this economic cycle. Also noteworthy is that the curve has inverted during a cutting cycle, rather than a hiking cycle.

2s10s Spread:

Source: Bloomberg, EPB Macro Research

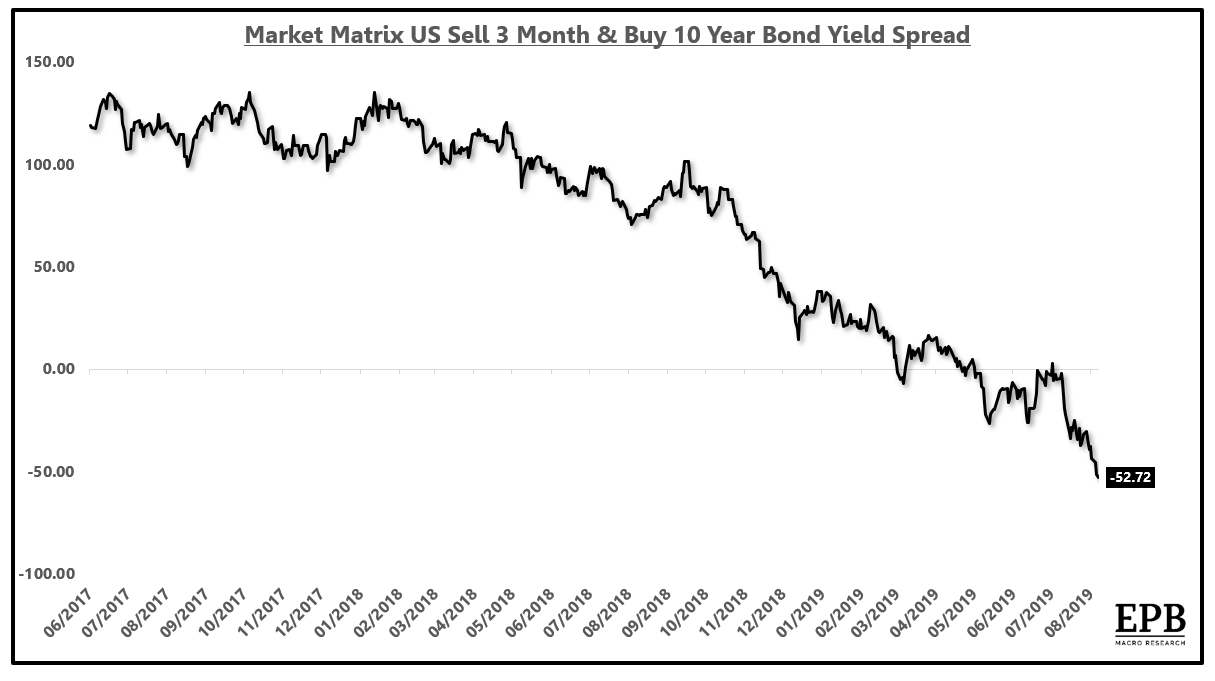

The 10-year yield has fallen a full 50bps below the 3-month rate, a clear indication that the market is forecasting aggressive rate cuts, even if the Federal Reserve is not yet on board.

10-Year Yield Minus 3-Month Yield:

Source: Bloomberg, EPB Macro Research

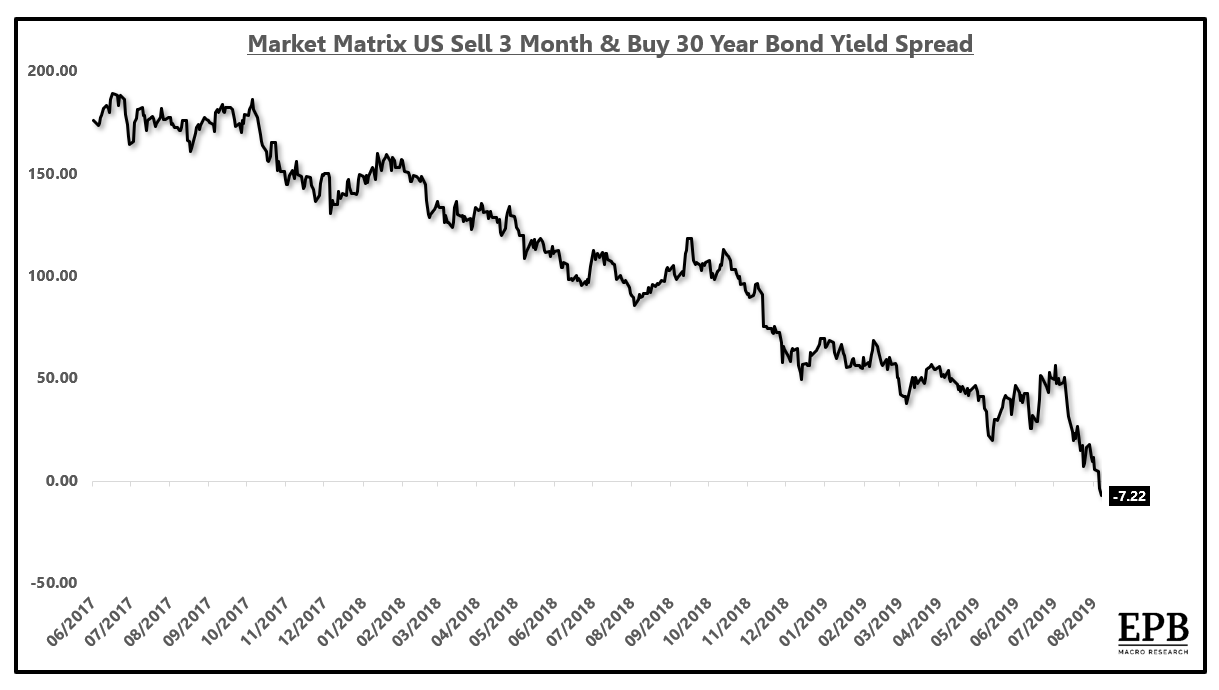

The entire yield curve is now inverted with the 30-year rate 7bps below the 3-month bill.

30-Year Yield Minus 3-Month Yield:

Source: Bloomberg, EPB Macro Research

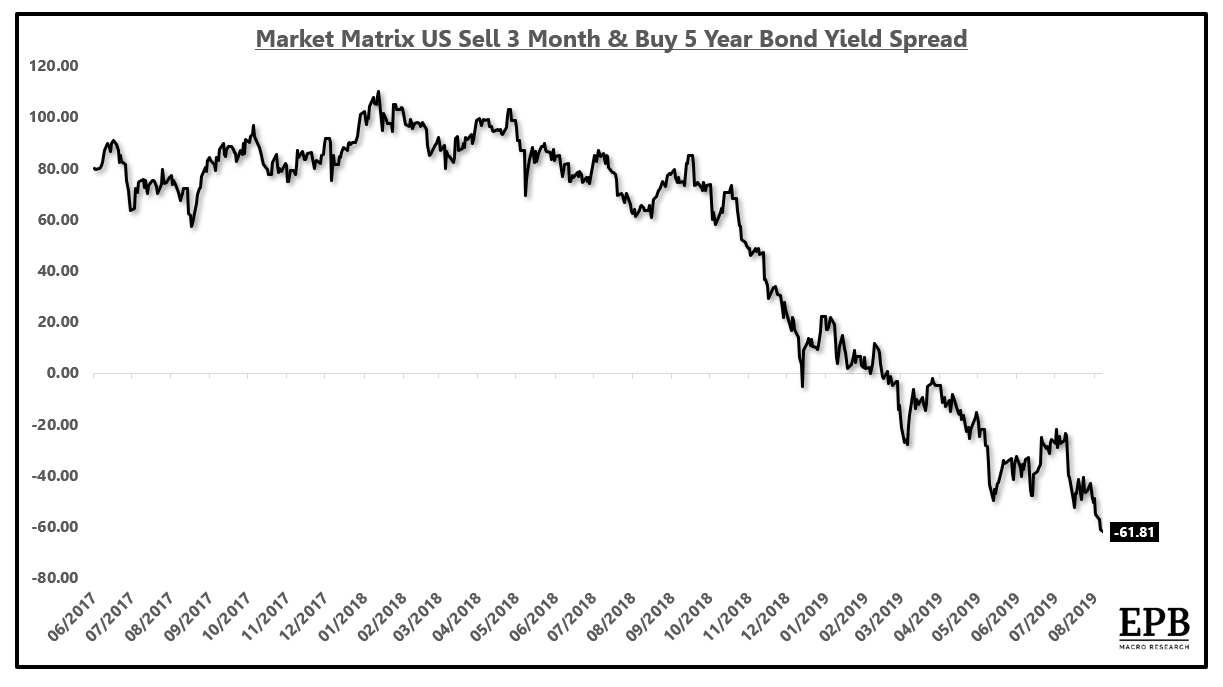

The belly of the curve is massively inverted with the 5-year yield over 60bps below the 3-month yield.

5-Year Yield Minus 3-Month Yield:

Source: Bloomberg, EPB Macro Research

The Fed has a lot of heavy lifting to do if their intention is to "un-invert" the yield curve.

One, two, or even three rate cuts from here is still likely to prove insufficient in bringing the entire curve out of inversion territory.

Starting with the growth rate cycle slowdown in early 2018, amplified by the separate but overlapping inflation cycle downturn starting in the fall of 2018, the move in long-term rates was quite predictable.

The Federal Reserve was roughly 10 months late to the first rate cut, after two mistaken rate hikes in September and December of 2018.

Long term bonds are now up more than 30% year-to-date and have risen by nearly 50% since November 2018.

{kind=link}

{kind=link}

{kind=link}

{kind=link}