Market Analysis for Jul 5th, 2021

By

Rida Morwa

By

Rida Morwa

Summary

- Our Portfolio has closed the first 6 months of 2021 with stellar results.

- I highlight our current investment strategy, and how we are positioning ourselves for the next 12 months to achieve similar returns.

- Inflation pressures are set to remain high for the next years to come.

- This bull market is set to continue strong – despite several risks we could be facing, including higher inflation, new COVID variants, and future Fed rate hikes.

- We are in a raging bull market that offers significant returns over the next two years.

The first 6 months of 2021 are officially over and they come with a stunning performance of our "Model Portfolio" – beating the 15.2% return of the S&P 500 index by over 50%! This has been our best performance for a half-year period since 2016. Our calculated strategy has paid off handsomely. Since the beginning of the year, we have positioned our portfolio based on 4 main themes:

- Overweight economically sensitive stocks, including cyclical ones, with a view that a "supercharged economy" is underway, with such sectors to be the main beneficiaries.

- We have been overweight "value stocks" and underweight "growth stocks" with a view that "value stocks" are the first beneficiaries during any economic recovery. This strategy has paid off handsomely as "value stocks" have had their best performance in over a decade.

- Our portfolio is mostly focused on U.S. companies with our expectations that the U.S. economy is set to be the first and strongest economy to recover among the developed nations. This is exactly what happened, and continues to unfold. We still strongly favor U.S. equities and see much more upside potential.

- We are also overweight smaller cap U.S. companies or companies with exposure to U.S. small and medium businesses. The COVID relief and economic stimulus plans have resulted in strong tailwinds to many of our picks, such as Newtek (NEWT) returning 83% for the first half of the year, America First Multifamily Investors (ATAX) returning 63%, and Iron Mountain (IRM) returning 48%.

- We also added inflation-resistant stocks since the beginning of 2021 as we expected that strong consumer demand across the globe will result in higher commodity prices, translating into an inflationary environment. Our expectations in this respect have paid off well too.

Our strategy for the rest of the year will remain mostly the same, with more focus on companies that are set to benefit from widening interest rate spreads as the Fed insists on keeping short-term interest rates near zero, while longer-term interest rates (such as the 10-year and the 20-year Treasuries) head higher due to higher inflation expectations. As a reminder to our members, households’ expectations for inflation in the coming 12 months have shot up to 4.6%, according to the University of Michigan’s consumer survey implying that inflation next year is set to be much higher than most expect.

Growth stocks have been seeing strong momentum as I have outlined in my last market outlook, due to two main factors including statements from the Federal Reserve that Fed Fund rates will not be hiked until the year 2023, and the prospects of meaningful higher corporate taxes are off the table for now. The U.S. just won international backing for a global minimum tax of 15% on large global companies which is already a big achievement for the administration. Note that growth stocks are set to suffer the most from rising short-term interest rates.

While I am not bearish on growth stocks, these growth stocks are "deflation beneficiaries" and their strong rally last month is unlikely to be sustained. As inflation starts to kick back again, growth could begin to underperform as leadership goes back to favor the Value and Cyclical stocks, including the high dividend stocks we are invested in.

About Commodities and commodity-related stocks, we also saw a knee-jerk reaction this past month. However, they have started to rally again, as the markets are almost always forward-looking, with real demand for scarcer resources, coupled with expectations of persistent inflation. Our portfolio has good exposure to commodities and commodity-related stocks, and provides us with a good hedge against inflation to preserve both our "income purchasing power" and the "value of our invested capital, inflation-adjusted".

The Week in Review

The week ended up on a very strong note, which the media mostly attributed to a strong jobs report. The U.S. labor market keeps accelerating with employers adding 850,000 jobs in June – the biggest gain in 10 months – and workers’ wages rose briskly. Hourly wages among private-sector workers rose 3.6% from a year earlier. However, contrary to what the media is telling you, this would be pretty bearish news for equities because it means that the economy is starting to overheat, and inflation will rise faster than expected, which will prompt the Fed to hike interest rates even earlier than the year 2023.

Perhaps, the biggest piece of good news for equities was that the unemployment rate, derived from a separate survey of households, rose to 5.9% in June from 5.8% in May. This is because a small number of Americans came off the sidelines and entered the job search, expanding the labor pool. This will at least ease the pressure on the Fed for a while.

The Job Numbers Reflect 'Scary Inflationary Pressures'

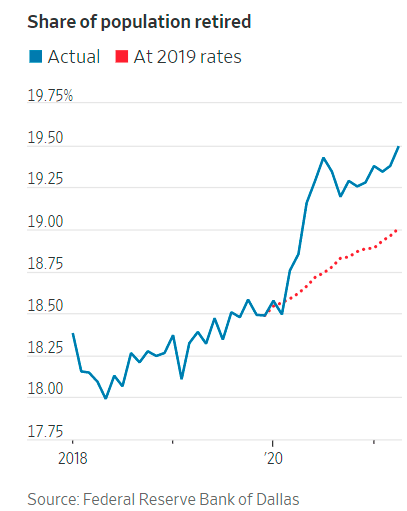

Disregarding the increase in the unemployment numbers which is most likely a "one-time adjustment", the tight labor market looks pretty scary as far as inflation is concerned. The excess liquidity in the system has resulted in "too much money chasing the same goods and services." Add to this supply disruption, and labor shortages due to many Americans taking early retirement following the COVID pandemic. According to the Dallas Fed, roughly 1.5 million more people retired during the pandemic than would have been expected before the onset of Covid-19—meaning fewer available workers to take open jobs as the economy reopens.

Because of the retirement wave, the labor market could reach full employment before that gap in employment requirements has been fully made up.

These figures have actually puzzled the Federal Reserve itself. Jerome Powell in a press conference stated on Wednesday:

This is an extraordinarily unusual time, and we really don’t have a template of any experiences of a situation like this....We have to be humble about our ability to understand the data....We don’t actually know exactly what labor-force participation will be as we go forward.”

The increase in wages alone looks pretty scary without factoring in other inflationary pressures coming from higher commodity prices, transportation and storage costs. Unfortunately, inflation is always ahead of wage increases,

Unfortunately, increasing wages (in our case 3.6% year-on-year) always lag inflation, and therefore we can fully expect to see inflation creeping higher.

In fact, former PIMCO CEO El-Erian commented on this situation this week in an interview on CNBC:

This supply disruption could contribute to a "cascade" of inflationary pressures.

Mr. El-Erian worries that inflationary expectations could rise, turning transitory price changes into long-term inflation. He said the most dangerous situation would be if the Fed moved too late to halt inflation.

While I agree with Mr. El-Erian about "non-transitory" inflation pressures, unfortunately, the Fed has little ammunition (or interest rate hikes they can use) to fight inflation. The Fed has indicated (for now) that they will keep the last bullets they can use until the year 2023, which might be their best strategy given the current circumstances. My views are that the first rate hikes will likely be in late 2022, but will still not make much difference to curb inflation.

People relying on Social Security, pensions, and bonds lose the most as consumer prices increase. This is especially true if they don’t own a home, or have significant other inflation-protected assets.

Main Risk to the Inflation Pressures

As I highlighted in last week's market outlook, the main risk to the inflation thesis is another round of new COVID-19 variants that would result in new lockdowns and economic shutdowns. The data so far indicates that the spread of the Delta variant has on average coincided with an improvement of the overall COVID-19 situation in affected countries suggesting that the vaccines are working efficiently in the vast majority of cases, and hospitalization rates remain low. As long as the healthcare systems are not overwhelmed, shutdowns will not be on the table.

Even if we are faced with new shutdowns, this would not impact the Bull Market thesis, as investors will have even more liquidity to invest in equities due to a lack of spending opportunities. Furthermore, investors have learned from the last market crash that if we see any new liquidity crunch, the Fed will come to the rescue once again, and most investors will just buy the dip.

A Liquidity Driven Bull Market That No Bad News Can Stop

Despite all the inflation, employment, and new COVID variant worries, trying to analyze the short-term market moves in this strong bull market is not very relevant. As I have been emphasizing over the past several months, this bull market is one that is driven by high liquidity, trillions of cash on the sidelines, and more liquidity being injected into the markets.

No bad news is going to derail this market. This is such a strong market that will keep dismissing bad news and will continue to climb higher regardless of the economic conditions, as long as there is a mountain of money that is still waiting to be invested.

For our newest members who are wondering why the Fed has little tools to fight inflation, I would recommend reading the Market Outlook dated June 13, 2021, and entitled "The Great Inflation Lie".

The beauty of investing in our high dividend stocks is that when your portfolio is yielding over 7%, you are already beating inflation, even without re-investing your dividends. By re-investing them, you would be compounding your future returns. Investing in the right dividend stocks will provide you further hedges, price appreciation, and more income for your retirement.

Technical Situation

The market closing on an all-time high on a Friday before a long weekend can tell you a lot about how strong this market is today. Usually, on long weekends, traders and large institutional investors tend to close their positions ahead to reduce risks due to unforeseen events. Yet, this has not happened this week, not even when the markets are at all-time highs. No profit-taking, almost like there are no worries about anything going wrong.

The closing on Friday sums up exactly what this bull market is about, and it is all about "excess liquidity". It is like "no matter what happens", this market will continue to go up. No bad news can bring it down unless the excess liquidity "dries up" and this is not happening anytime soon.

Going back to the technicals, all the stars are aligned for higher highs. With the S&P 500 index above the 4350 level, the next target for the index is at the 4400 level or 2.3% higher from here, and we are likely to see this upside coming soon.

To the downside, the support for the S&P 500 index is at the 4200 level which corresponds to the 50-day moving average, and next comes the 4000 level which I believe would be a “floor" for the index with plenty of buying pressure below.

Note that as with most summer seasons, trading is thin, and we can expect "volatility" to hit us anytime. I would consider any pullback resulting from such a situation to be an opportunity to add positions to your portfolio.

Longer-Term Market Outlook

We have not been seeing any significant market pullbacks over the past 12 months, mainly due to "deep pocket" investors buying each and every dip. While the markets may struggle, or see a consolidation pattern, once we reach the 4400 level for the S&P 500 index, once we break above, the next target would be the 4600 level for the S&P 500 index (or 5.7% higher from here). I expect we will reach this target over the next 6 to 12 months, if not earlier.

Conclusion

We remain in an environment where excess liquidity is the main theme. There remain trillions of dollars of "money sitting on the sidelines" and is only set to get much bigger. Global government infrastructure spending on roads in the largest world economies (including, roads, inter-continental highways, ports, trains, 5G, "Electric Vehicles" and "less polluting" sources of energy will inject further trillions into the global economy. We are also on the brink of a multi-year capital spending boom on numerous fronts with global capital expenditures to reach over $5 trillion over the next five years. Borrowing will remain cheap as the problem of rising short-term rates will balloon the overall deficit and will have objections from various governments.

High Liquidity and cheap money are set to drive equities much higher over the next two years, with economically-sensitive and inflation-resistant stocks being the biggest beneficiaries.

It is one of the most exciting times to be invested in the markets! I am very excited about the prospects of our portfolio over the next 24 months and looking forward to strong outperformance, much higher than the market indexes will offer, together with high yields and recurrent income.

Due to the long holiday weekend, our "Best Picks of the Week" report will be posted tomorrow, on Monday. Stay tuned.

Wishing you a happy long 4th of July Weekend!

Rida MORWA