Market Analysis for Aug 16th, 2021

By

Rida Morwa

By

Rida Morwa

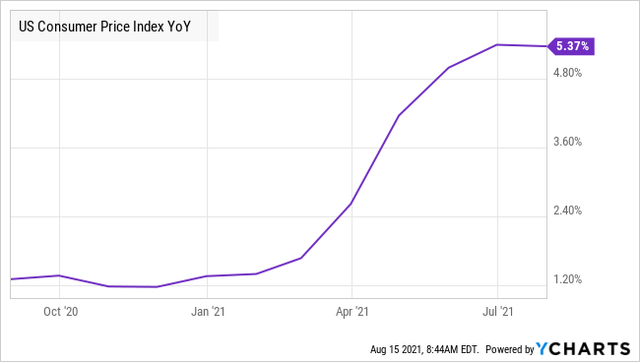

The highlight of the week was the inflation figures. The Consumer Price Index (or CPI figures) came out on Wednesday and showed an increase of 0.5% last month after climbing 0.9% in June. In the 12 months through July, the CPI increased 5.4%, at their 13-year high on a yearly basis. Wednesday's CPI numbers were generally interpreted as evidence by both sides. The transitory crowd pointed to the overall CPI being roughly in line with expectations and significant slowdowns in some areas like "used cars and trucks" being up only 0.2% in July, compared to +10.5% and 7.5% the prior two months.

Our big concern at HDO was never about used cars, trucks, or individual items. Last month, we were told by the Fed that we shouldn't worry about inflation because used cars accounted for more than 1/3rd of the gain. Is it really a big deal for most people if used car prices go up? Well, it is for those who cannot afford to buy a new car.

Then in July, used cars reduced the headline inflation number, coming in below average but still increasing by 0.2%. So the largest driver of inflation in June (used cars) essentially remained steady in July . . . Yet inflation was still up 0.5% month/month – which, if annualized, comes to over a 6.1% inflation rate!

The Reason For Soaring Inflation?

Rent, energy, and food all continued to push higher at a similar or higher rate than they did in June. We talk about inflation as being 5% over the past year, but we should keep in mind that over the past year, inflation was relatively tame. The increase has primarily occurred since April. Here is a look at CPI over the past 12 months:

Inflation was never centered around used cars. Are there items that will shoot up and fluctuate from month to month? Absolutely. What is going to drive permanent inflation is not the variability of a handful of random goods. The factors that will drive inflation are higher rents, higher wages, and higher input costs for manufacturers. These are all more "sticky", once they go up, they don't come down so easily.

PPI Leads CPI

This is where the "Producer Price Index" (or PPI) comes in. This is a measure of the prices received by the original producer. It measures the first commercial transaction for goods and services. It came in at 7.8%, up 1% in just one month. Consumer-facing sellers are not always willing, or even able, to immediately pass rising prices to the end-consumer which is what CPI measures. They have to face the reality that you might compare prices with competitors if you want to buy something.

However, if the input prices represented by the PPI are sustained, they will eventually work their way into consumer prices. Businesses are often willing to overlook temporary price jumps for raw materials. They might eat a loss for a month or two, to make customers happy. What we like to watch are the permanent expenses, the ones that won't go away.

For example, rent. Businesses sign rental contracts that can be 5-7 years. If rent goes up, it doesn't go down very often. An under-reported fact from the July PPI is that non-residential rents went up 2.2% from June to July. This compares to 1.1% from May to June. It is up 3.9% year over year. In other words, rents were mostly flat and in the past two months have shot up over 3%. With low interest rates spurring on real estate prices, this is a trend we expect to continue and accelerate.

Prologis (PLD), a company that rents industrial warehouse space, reported rent increases of 15.5% on a cash basis and 31.5% on a GAAP basis. In other words, the higher rent today is only a fraction of how much rent will go up over the course of the lease. Companies like Amazon (AMZN) are happily signing long-term contracts with materially higher rent. It is only a matter of time before these costs work their way to consumers.

Rent and labor are often two of the largest fixed expenses for producers, and both of those are heading up.

Dividend Stocks Are Highly Attractive

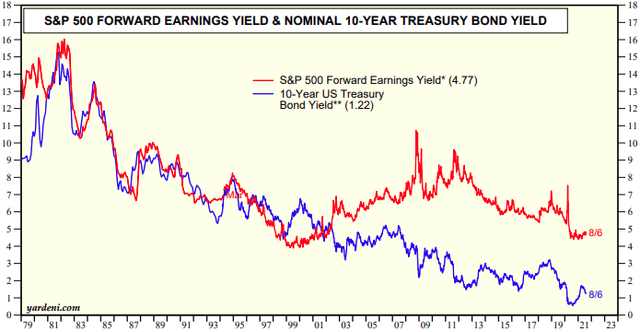

Today's bull market remains a liquidity-driven one with money flowing into both U.S. stocks and bonds. One big reason that U.S. Treasury yields have remained so low in today's environment is that many foreign investors have the choice of either investing in negative Treasury yields from their own nations, or get a slightly positive yield from U.S. Treasuries. This has resulted in the 10-year Treasury yields remaining as low as 1.3% today.

Despite the big rally in the equity markets that we have seen over the past two years, equities remain cheap. As I have stated in many previous market outlooks, one of the best valuation metrics for equities is to compare the "earnings yield" of equities to the "earnings yield" of the 10-year Treasuries. The S&P 500 index earnings yield is at 4.77% compared to 1.22% for the 10-year Treasury. Based on this ratio, equities are around their cheapest valuations in decades.

Source: Yardeni.com

This is the power of a liquidity-driven bull market that I keep referring to in my market outlooks.

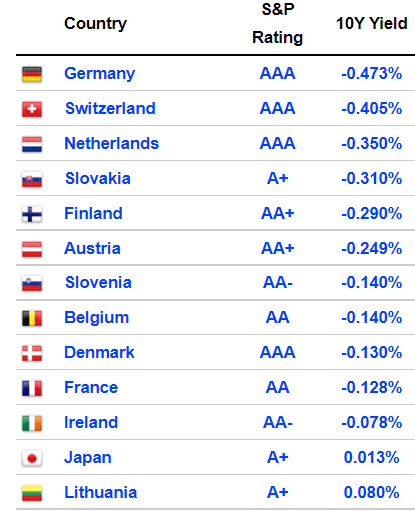

The case for dividend stocks is even stronger. The reality is that U.S. investors holding cash in the bank or fixed-income are pouring into the stock market in search of higher yields. Bond yields today, even junk bonds, are providing you with negative returns, inflation adjusted. Furthermore, negative interest rates across the globe are driving foreign investors' money to the United States, and notably hunting for dividend stocks. Remember, negative or zero yields in Europe and East Asia are common, and investors are pouring money into the U.S. to get any sort of positive yields. Here is a list of some counties with negative or near-zero Treasury Yields:

Source: worldgovernmentbonds.com

Imagine investing your money for 10 years to seeing it depleting at a rate of 0.5% each year! This is the case in Germany. Even worse, inflation in Germany is currently running at 3.1%, so they are effectively losing 3.6% on their 10-year Treasuries in 2021 alone. I fully expect more international investor money to keep moving to the U.S. and hunting for dividend stocks.

Our "Core Portfolio" provides a perfect solution today by offering an average yield of +7%. Higher demand for solid dividend stocks will result in higher prices and capital gains for our portfolio.

With new "Buy Alerts" this week, that overall yield will improve this week. Stay Tuned!

Stay on the Defense with Value Stocks!

With inflation soaring and COVID scares likely to increase, it is best to stay focused on those sectors that are the most undervalued and least overcrowded. This is the best line of defense and the way to win with a view of 12 to 24 months. Note that I continue to expect that pullbacks will remain shallow, but sector leadership will not be the same.

As a result of higher inflation and higher inflation expectations, the 10-year treasury yields have climbed up again to the 1.3% level, close to its highest in the 3 weeks.

I expect the 10-year Treasury to recover to at least 1.5% to 1.7% by year-end due to continued inflation pressures and with long-term interest rates starting to factor in higher cost of living expenses. The 10-year yield will continue to remain low relative to its historical norms due to two factors:

- High level of cash chasing the 10-year U.S. Treasuries.

- The Fed is not expected to raise short-term rates, which in turn puts downside pressure on longer-term rates.

Still, I believe that Treasury yields have bottomed. With a higher Treasury yield, I expect "growth stocks" to start lagging again, and that we will witness a new rotation toward more economically sensitive sectors where value stocks will outperform once more. Note that higher long-term rates hurt growth stocks, but not "value stocks". Growth stocks' valuations depend on the time value of money which shrinks as interest rates go up. Value stocks are mostly valued on the earnings they generate today rather than tomorrow, and therefore tend to outperform in periods of inflation and higher interest rates.

Note about Smaller and Medium Cap Stocks

Smaller and medium cap stocks tend in general to be mostly "value stocks". They are currently having one of their strongest Q2 earnings season with 75% of them beating estimates by +25%. Smaller cap companies, especially U.S. companies, have outsized leverage to the economic recovery with growth estimates well above the S&P 500 index for both the years 2021 and 2022. This is one reason why we favor smaller and medium cap stocks in our "model portfolio".

These stocks have been soaring since October 2020, however they started to consolidate in June 2021. Today, their valuation is very attractive relative to the S&P 500 index given both its lower valuation and growth potential. Now is a great time to average down on those smaller cap stocks that have pulled back some, or to start new positions. I expect these stocks to strongly outperform as pricing catches up to their strong fundamentals and increased earnings guidance. Examples of smaller cap stocks include:

- Our BDC stocks: ARCC (ARCC), CSWC (CSWC), ORCC (ORCC)

- Our Mortgage REITs: AGNC (AGNC), NLY (NLY), BRSP (BRSP)

- Our CLO stocks: ECC (ECC), OXLC (OXLC), XFLT (XFLT).

- Our Property REITs: HTA (HTA), BRT (BRT)

I particularly like the above sectors in the current environment as they provide the most exposure to the U.S. economy in terms of both growth and high income. The good news is that most are inflation resilient too such as BDCs, CLOs, and REITs.

The Cheapest Stocks and Sectors Today

In addition to "Value Stocks" set to outperform going forward, at HDO we like to target cheap stocks and sectors that have strong fundamentals.

1- First, let us have a look at those sectors that are the least overcrowded.

According to a Citibank study, technology, semiconductor, and software stocks are some of the most crowded sectors, even though their performance has not been that great lately.

Some of the least overcrowded sectors include utilities, REITs, healthcare, industrials, and financials. As our members know, these are some of our most favorite sectors.

Conventional thinking is to avoid buying crowded stocks because they may become harder to attract marginal investors. Less crowded stocks will react more positively to fundamental catalysts, as they attract new investors on positive news. On the other hand, investing in crowded sectors can be dangerous in case of bad news as big money starts pulling out of the sector generating large pullbacks.

Note that following under-crowded sectors alone is not enough by itself. In a strong bull market like today, at HDO, we like to look at valuations too.

2- So as a 2nd step, let us have a look at those sectors that are the cheapest:

The following five sectors are looking pretty cheap compared to their pre-pandemic Price/Earnings ratio level (or in February 2020):

One big reason why these sectors are trading below or close to their previous P/E ratios is that either:

- They have seen a big improvement in earnings. This is notable in the Industrial, Materials, and Healthcare sectors.

- They pulled back recently due to temporary factors. This is the case of the Financial sector which has pulled back due to the decline in the 10-year Treasury yield. I expect the Treasury yields to move higher by year-end as noted above. This would be bullish for the Financial sector, especially given that this represents today one of the least expensive sectors in today's market.

Note that the Utilities sector (XLU), although not as cheap as the five sectors above, it is not very expensive. This sector is likely to continue to see high demand as investors dump Treasuries and invest in utilities for higher yields. Utilities are viewed as a defensive sector because they make money both in good and bad times (recession resilient sector), and offer both yield and some growth – a much better alternative to Treasuries.

Based on the above analysis, and taking into account valuation and crowded traded factors, I am mostly bullish on those HDO picks with exposure to these sectors:

- Financials: John Hancock Financial Opportunity Fund (BTO) yield 5.1%

- Healthcare: Tekla Healthcare Investors (HQH) yield 7.5%, and Tekla Healthcare Opportunities Fund (THQ) yield 5.5%

- Industrials and Materials: BlackRock Resources & Commodities Strategy Trust (BCX) yield 5.1%

- Energy: Blackrock Energy & Resources Trust (BGR) yield 5.1%

- Utilities: Reaves Utility Income Fund (UTG) yield 6.3%, and Cohen & Steers Infrastructure Fund (UTF) yield 6.2%

The above sectors and picks also have strong fundamentals, with financials, industrials, materials, and energy being economically sensitive sectors (and inflation resilient), while healthcare is a booming sector with strong tailwinds. Finally, the Utilities sector is a defensive one that is set to benefit from the infrastructure bill and from the "hunt for yield".

The bottom line is that treasury yields should continue to rise, resulting in "economically sensitive stocks", commodity stocks (including energy stocks), and value stocks strongly outperforming.

The Technical Situation

The technical situation cannot be looking better. The bullish trend is tremendous, and disregarding all the macro-driven factors, is spectacular. The S&P 500 closed the week at the 4,468 level, a new all-time-high. After that, the index is likely to go higher towards the 4500 level, and ultimately towards the 4600 level which is likely to happen relatively soon.

What is very interesting this week is that the S&P 500 index saw 3 trading days of new record highs. And so far this year it has made 47 new record highs. History shows us that when this happens, it means that we are in the midst of the very strong bull market that is set to continue.

On the downside, the major support is at the 4300 level which corresponds to the 50-day moving average, and has been a reliable support for the past 10 straight consecutive months. Every time the index dips close or just below the 50-day moving average, investors buy the dip!

Having said that, we may see some consolidation when we reach the 4500 level, which is much needed at this stage. So it is possible that we may see the index test back to the 4300 level or just below. I believe that if that happens, it would be followed by a very swift recovery, as "value hunters" will step back in again to put new money to work.

My best advice in case we see some volatility is to keep a long-term view and not to time this market. This is a market that is ultimately going to find reasons to go much higher regardless of any transitory factors or "market scars" such as COVID or fluctuations in Treasury rates. This is the beauty of a "liquidity-driven" bull market that is financed by government spending, excess savings, low interest rates, and lack of other investment opportunities. Last but not least, do not underestimate the impact of inflation that is eating away investors' savings in their bank accounts. Smart investors are pulling their money out and putting it to work into equities and real estate to fight off the impact of inflation. All these factors will continue to act as strong tailwinds to equities.

The Bottom Line

Do you feel everything is getting more expensive while the purchasing power of the dollars in your bank is shrinking? Many do, and this is why "asset values" are soaring because smart investors getting rid of their cash.

Yes inflation is soaring, and the Fed wants to eat your money to reduce debt levels. Your cash is trash. You need urgently to get your money working for you and fight this trend. I touched extensively on this point in a market update two weeks ago. If you did not have the chance to read it, the following is the link:

The Fed Wants To Eat Your Money, And Cash Is Trash

The good news is that the future looks bright if you are invested in the right stocks and sectors. We remain in a strong and unstoppable bull market driven by high liquidity which is financed by government spending. I remain confident that we are set for a multi-year global economic and market expansion financed by the U.S. Government and others across the globe. This market is set to reward long-term investors, regardless of any short-term market fluctuation that we may see. It is not too late to act now. When inflation is flaring, you don't want to be the last person holding cash!

I invite you to take a 15-day free trial to our service you will have access to our model portfolio targeting a +9% yield by investing in dividend stocks, bonds, and preferred stocks.