Sentiment Speaks: 4300+ Here We Come

This article will be published after I return from Passover next week:

This market seems to have confounded most investors and analysts over the last year. While many reasoned that the market crash in March 2020 was due to the Covid crisis, many who held such beliefs had no real explanation for the incredible rally off that March 2020 low which has now seen the S&P500 almost double in one year. In fact, that rally was occurring even though the worst news of the Covid death toll was being reported, along with the highest unemployment numbers in history, which was being caused by economic shut-downs across the country.

How can the market possibly rally, and especially in such a strong fashion, in light of all the issues the economy was facing regarding Covid?

Do you not get it yet that Covid was an excuse for the decline, whereas it did not matter during the rally? And, yet, I still see article after article trying to “splain” how Covid will affect the market. And, if you still think that Covid matters to the market, then you really have not been paying attention or you simply own some of the best blinders sold on the market.

Now, there are some of you that may attribute this rally to the Fed’s actions. But, I think that is a very superficial view of the market, especially in light of the facts.

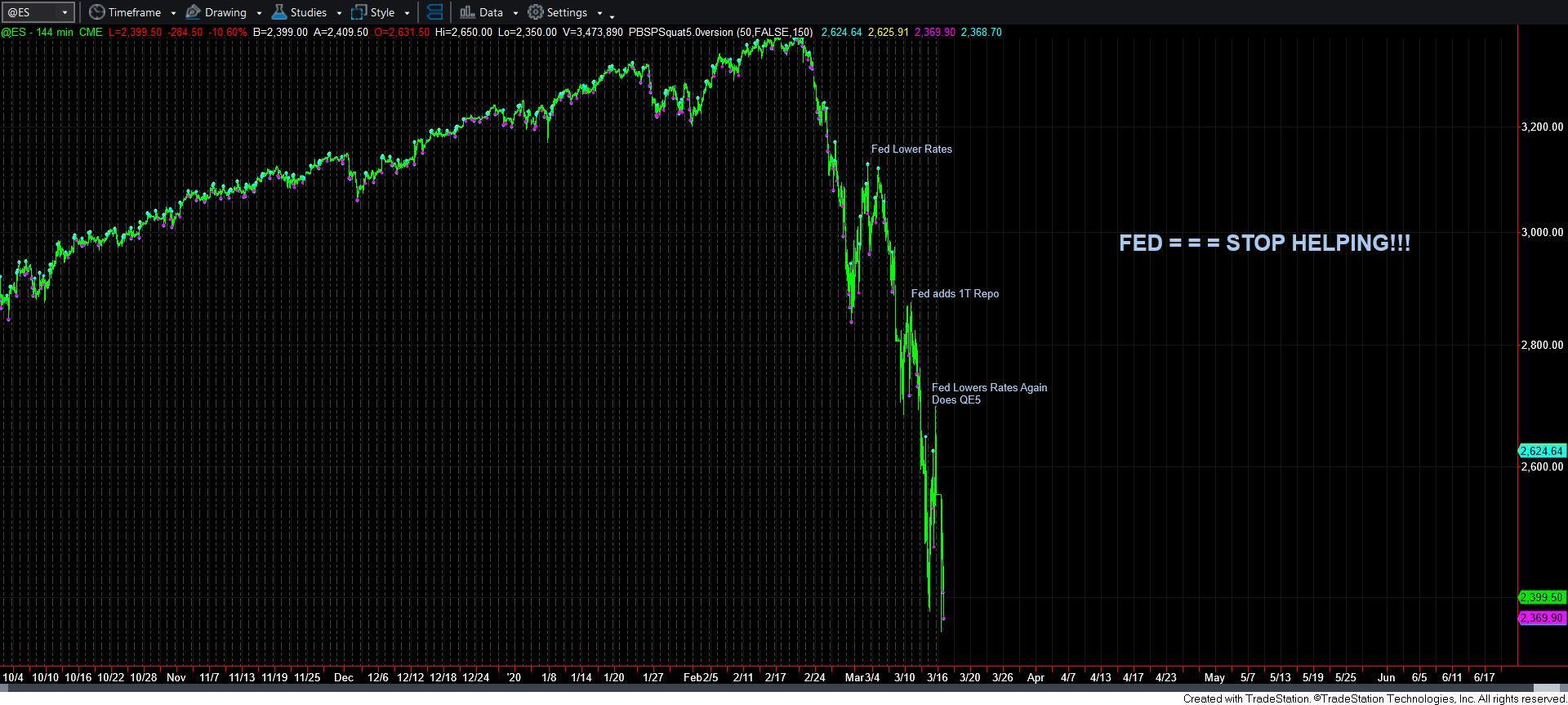

You see, the Fed did not just act at the bottom of the market in March 2020. In fact, they acted 3 times before we even struck the bottom, with each action being met with even more intense selling, as you can see from the chart above. So, if you are really assuming that the Fed has the power to “cause” this rally, then why did the rally not begin after the first Fed action? Or even the second? Or even the third?

In fact, if you really believe the Fed “caused” the rally with its actions at the March low, do you also believe that the Fed “caused” the decline with each of its actions on the way down? If not, why not? I mean, just look at the chart and the timing of each of the first three Fed actions during March. Is this not based upon the same “logic” with which you claim that the Fed “caused” the rally?

If you are being honest with yourself, then you would recognize many market participants and analysts maintain a perspective that is no different than the one maintained by my children when they were 5 years old when we were stopped at a traffic light. They used to look at the red light, and say “now,” as they try to time the light changing back to green. And, if it does not change, they would again say “now.” And, this goes on for maybe another 5 to 10 times, depending on how long the light takes to change. When the light finally changes at one of their “now’s,” they proudly assume that they caught that timing ever so perfectly.

Applying that same example to those who believe the Fed caused the market to rally would suggest that each Fed action in March was akin to my children’s “now.” And when the market finally bottomed and began to rally after the 4th “now,” all of you were just as proud as my children in thinking you caught that market timing ever so perfectly, and that it was so clear to you that the Fed “caused” the rally. Seems kind of foolish when you look at it that way, does it not?

So, the honest question you need to ask yourself is if you want to look at the stock market as would a 5-year-old child?

I can tell you that the former Chairman of the Fed, Alan Greenspan, does not. He understood why the market bottoms with a much more mature perspective about how the stock market really works:

“It's only when the markets are perceived to have exhausted themselves on the downside that they turn.”

Still, I know many of you will simply shake your head at what I present here, and just discount my perspective as being based upon some “voodoo” market theories, since it goes against all “reason.” Well, not only have my theories allowed me to accurately identify most major turning points we have seen in the market for many years, my theories are actually supported by many recent studies being conducted about the market over the last 25 years, wherein they have been noting that exogenous factors do not have nearly the affect upon the market as the majority believes.

For example, in a paper entitled “Large Financial Crashes,” published in 1997 in Physica A., a publication of the European Physical Society, the authors, within their conclusions, present their understanding of how financial markets are really driven:

“Stock markets are fascinating structures with analogies to what is arguably the most complex dynamical system found in natural sciences, i.e., the human mind. Instead of the usual interpretation of the Efficient Market Hypothesis in which traders extract and incorporate consciously (by their action) all information contained in market prices, we propose that the market as a whole can exhibit an “emergent” behavior not shared by any of its constituents. In other words, we have in mind the process of the emergence of intelligent behavior at a macroscopic scale that individuals at the microscopic scales have no idea of. This process has been discussed in biology for instance in the animal populations such as ant colonies or in connection with the emergence of consciousness.”

In simple terms, the market is not a “reasonable” environment, but an emotional or biological one.

And, if you are having a hard time accepting these concepts about the workings of the market due to your old, and potentially outdated, perspective about the market, consider that it was once widely believed that the earth was flat.

In my last article, I was looking for a market pullback to test the important 3850SPX support region – at least as I saw it. And, when the market provided us with the expected pullback to the support target (it bottomed at 3853SPX), pundits and analysts began to scour the news as to the cause of the pullback I told you was coming. Yet, the pullback did not have an obvious cause evident in the news feeds, which left many scratching their heads. One of my members posted this statement he found in an article published that evening:

"Stocks extended losses in the final hour of trading, but analysts said there was no clear catalyst for the move." March 23, 2021

If you are being honest with yourself then you would recognize that all this author was saying is that he scoured the news reports and could not find a superficial reason he could pin the decline upon. Remember, this is how most “analysis” is provided today within the media. They see a market movement, and then scour the news to find the “cause.” If this really was an appropriate manner in which to analyze the market, then you would have to come to the logical conclusion that the market should never move unless there is an associated “reason.” Therefore, action like that seen on March 23rd should be impossible.

So, are you being honest with your own market perspectives?

And, let’s not forget that I told you that I expected a pullback before it happened, and that the pullback should ideally hold 3850SPX if we were going to rally to new highs sooner rather than later.

Folks, I am not trying to tell you that I have the holy grail that will tell me what will definitively happen in the stock market. Rather, I am trying to outline for you what will not and cannot work on a consistent basis in the market, and why it is even foolish to try. And, while that may make some of you think that I am presenting my case as a know-it-all, I really do not care. My point is to open readers’ eyes and minds as to what works and what does not work in the market.

So, rather than being based upon the superficial market perspective outlined above, our analysis is based upon a probabilistic mathematical methodology which attempts to track overall market sentiment in order to glean the next high probability market movement. Again, we are not providing you with certainties about market direction. We are providing you with higher probability expectations, and we do not base it upon foolishness.

While we are often accurate in identifying the market directional move within our primary expectation (our members track us as being 70%+ accurate), one of the strongest aspects of our analysis methodology is that it provides for objective and advanced warning about when an expectation will likely invalidate. For example, in my last update, I noted that as long as the 3850SPX region of support held, then we should be setting up to attack 4300SPX sooner rather than later. However, if we broke that support, then it opens the door to test the 3700SPX region before we set up to attack 4300SPX. And, as we now know, the market struck a low of 3853SPX on that pullback, and went on to hit higher highs.

Yet, most people approach market analysis from a perspective of “tell me what the market is going to do right now.” Well, we provide our perspective by ranking probabilistic market movements based upon the structure of the market price action. And, if we maintain a certain primary perspective as to how the market will move next, and the market breaks that pattern, it clearly tells us that we were wrong in our initial assessment. But, here is the most important part of the analysis at this point: We also provide you with an alternative perspective at the same time we provide you with our primary expectation, and let you know when to adopt that alternative perspective before it happens.

This is no different than if an army general were to draw up his primary battle plans, and, at the same time, also draws up a contingency plan in the event that his initial battle plans do not work in his favor. It is simply the manner in which the general prepares for battle. So, why should we not do the same when we approach the market?

Moreover, we provide objective price points at which we recognize that we have to move to our contingency plan, and we then move into that contingency plan without delay. This avoids the big losses that so many traders and investors often experience, which drags on your overall performance.

Now, for those that have been following me closely through the last year, you would know that I maintained a strong expectation that the market would bottom within the 2200SPX region, followed by a rally to 4000+. While many believed me to be crazy as I was reiterating that expectation during the pinnacle of the market panic as we were striking the 2200SPX region in March of 2020, we are now at the 4000SPX region. Yet, the overall structure with which the market rallied off the March 2020 lows suggests that we can still rally as high as the 6000 region in the coming year or two. And, I see nothing to change that expectation at this point in time.

In the meantime, I would urge you to move on from sitting at the traffic light with my 5-year-old children and proclaiming “now,” as I would gladly invite you to begin to develop a more mature perspective on how the financial markets really work.